FHA financing can make a manufactured or mobile home purchase more realistic for buyers who want a lower down payment and flexible qualification standards. But FHA approval is not just about your credit score. The home itself, the foundation, the land arrangement, the title records, and the condition of the property all matter.

That is why FHA mobile home requirements are worth understanding before you choose a floor plan, sign a purchase agreement, or start looking at land. The right home can move smoothly through financing. The wrong setup can cause delays, extra costs, or a denial even if you are personally qualified.

One important note before we go further: in everyday conversation, many buyers say “mobile home.” FHA and most lenders typically use the term “manufactured home” for homes built to the federal HUD Code after June 15, 1976. That distinction matters because older true mobile homes often do not meet FHA manufactured housing standards.

FHA does not approve every mobile home

FHA loans are insured by the Federal Housing Administration, but they are made by FHA-approved lenders. That means two layers of approval usually apply. First, the property must meet FHA and lender requirements. Second, the borrower must qualify for the loan.

For manufactured housing, the property review can be more detailed than it is for a typical site-built home. Lenders need to confirm that the home was built to the correct standard, properly documented, safely installed, and acceptable as collateral.

According to HUD’s manufactured housing guidance, manufactured homes are built to federal construction and safety standards administered by HUD. For FHA purposes, that federal standard is central. If the home cannot be verified as HUD-code manufactured housing, it may not be eligible for the FHA loan path you want.

First requirement: the home must be a qualifying manufactured home

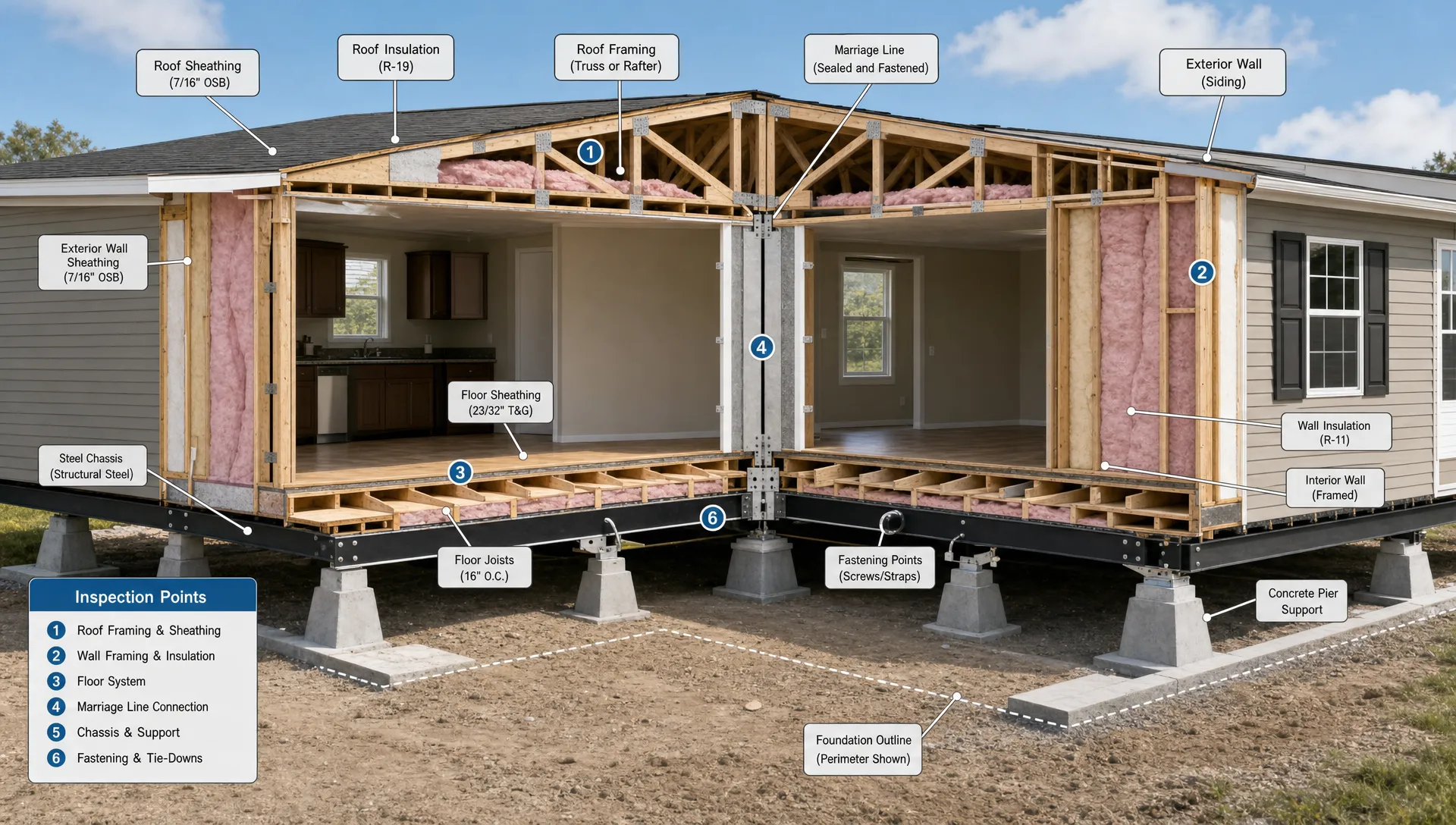

A key FHA requirement is that the home must generally be built after June 15, 1976, to the HUD Manufactured Home Construction and Safety Standards. Homes built before that date are usually considered true mobile homes, not HUD-code manufactured homes, and are difficult or impossible to finance with standard FHA manufactured home financing.

Buyers should also look for two important pieces of documentation: the HUD certification label and the data plate.

The HUD certification label, often called the HUD tag, is a metal label attached to the outside of each section of the home. A single-wide usually has one label. A double-wide usually has two, one for each section. The data plate is a paper label located inside the home, often in a cabinet, closet, utility area, electrical panel, or bedroom closet. It includes details such as the manufacturer, serial number, model information, roof load zone, wind zone, and heating and cooling information.

If the HUD label or data plate is missing, the deal is not always automatically dead, but it can become harder. Your lender may require verification from a source such as the Institute for Building Technology and Safety, which maintains manufactured home certification records. That takes time, so it is best to identify missing labels early.

FHA Title I vs. Title II: know which path you are using

FHA manufactured home financing is not one-size-fits-all. The two common FHA paths are often discussed as Title I and Title II. The right option depends on whether you are buying the home only, the land only, or the home and land together.

| FHA option | Common use | Property setup | Buyer takeaway |

|---|---|---|---|

| FHA Title I | Manufactured home, lot, or home and lot financing | May be used for certain home-only or leased-lot situations, depending on lender participation | Can be useful when the home is not being financed like traditional real estate, but availability varies by lender |

| FHA Title II | Mortgage-style financing for a manufactured home treated as real property | Usually requires the home to be permanently affixed to land and classified as real estate | Often used for land-and-home purchases, but foundation, title, appraisal, and site rules are strict |

Not every lender offers both options. Some lenders have additional requirements, called overlays, that go beyond FHA minimums. Before you shop seriously, ask the lender whether they finance manufactured homes, whether they offer FHA options for your setup, and whether they will finance the specific home type you are considering.

Core FHA mobile home requirements buyers should check

Although requirements vary by loan type and lender, most FHA manufactured home files involve the same major review points. Understanding these early can help you avoid choosing a home or site that creates financing problems later.

| Requirement | What it means | Why it matters |

|---|---|---|

| HUD-code construction | The home should be built after June 15, 1976, to HUD manufactured housing standards | FHA needs proof the home meets federal manufactured housing standards |

| HUD labels and data plate | The home should have exterior HUD tags and an interior data plate, or acceptable verification | Missing documentation can delay appraisal, underwriting, or approval |

| Minimum size and residential use | FHA generally requires the home to be at least 400 square feet and used as a primary residence | FHA manufactured home financing is intended for livable residential housing, not storage, vacation-only, or temporary use |

| Permanent foundation | For mortgage-style FHA financing, the home typically must be attached to an acceptable permanent foundation | Foundation issues are one of the most common manufactured home financing delays |

| Real property status | For many FHA mortgage transactions, the home and land must be treated as real estate | Title problems can prevent closing if the home is still recorded only as personal property |

| Site access and utilities | The property should have safe access, water, sewer or septic, electricity, and code-compliant utility connections | FHA appraisers and lenders need to confirm the home is safe, sanitary, and functional |

| Appraisal and condition | The home must meet FHA property standards and be acceptable to the appraiser | Repairs, health and safety issues, or unpermitted additions may need to be resolved before closing |

The biggest lesson: do not focus only on the home price. A home can look affordable but still fail FHA review if the foundation, documents, land status, or site conditions are not financeable.

Foundation and installation rules can make or break approval

For FHA Title II mortgage financing, the foundation is one of the most important requirements. The home usually must be permanently attached to a foundation that meets HUD standards, local requirements, and lender expectations. In many cases, the lender may request an engineer’s foundation certification, especially for an existing manufactured home.

A proper foundation is more than blocks under the home. FHA and lenders want to know the home is stable, safely anchored, and protected against movement. The towing hitch, wheels, and axles are typically removed. The home should be installed according to applicable standards, and the foundation should be able to support the structure long term.

Additions can also create issues. Porches, decks, carports, rooms, and roof structures may need permits or inspections. If an addition appears to affect the structural integrity of the manufactured home, the lender or appraiser may require further review. Even a nice-looking improvement can become a financing problem if it was not built properly or documented clearly.

For San Antonio buyers, this is especially important when comparing pre-owned homes on private land. A home may have been lived in for years without obvious problems, but FHA financing can still require documentation that was never gathered by a previous owner.

Texas title and real property rules matter

In Texas, manufactured home ownership records are handled through the Texas Department of Housing and Community Affairs. The TDHCA uses a Statement of Ownership to show important information about the home, ownership, location, and whether the home is treated as personal property or real property. You can learn more through the TDHCA Manufactured Housing Division.

This matters because FHA mortgage financing often works best when the manufactured home and the land are classified together as real property. If the home is still titled as personal property, additional steps may be needed before closing. The exact process depends on the transaction, lender, county, and ownership records.

If you are buying a manufactured home in a community where you lease the lot, your financing path may be different from a land-and-home purchase. Some leased-lot situations may be better suited to home-only financing or another loan type. If you plan to place a home on private land, the lender will also care about land ownership, access, utilities, zoning, floodplain status, and whether the site is ready for installation.

If you are still comparing placement options, Homes2Go San Antonio’s guide to mobile homes in San Antonio is a helpful next step. Buyers considering land and home together may also want to review the land and home package guide.

Borrower requirements still apply

Even if the home is FHA-eligible, the buyer must qualify. FHA loans are known for flexible standards, but they are not automatic approvals. Lenders review your credit profile, income, employment, debt, assets, and ability to repay.

HUD explains that FHA loans can help qualified buyers with lower down payment options, but the final approval still comes through an FHA-approved lender. You can review general FHA homebuyer information on HUD’s FHA loan page.

Common borrower factors include:

- Credit score and credit history

- Debt-to-income ratio

- Verifiable income and employment

- Down payment and closing cost funds

- Primary residence occupancy

- Mortgage insurance requirements

- Recent bankruptcies, foreclosures, or major credit events

Many buyers hear “FHA” and assume the property is the only challenge. In reality, the best results happen when the borrower and property are prepared at the same time. Getting pre-qualified before choosing a home can help you understand your payment range, possible down payment, and which manufactured home loan options are realistic.

Site requirements for land-and-home buyers

If you are buying land with the manufactured home, the site will receive close attention. Lenders want to confirm the property can legally and practically support the home.

In the San Antonio area, buyers should ask about zoning or land-use rules, deed restrictions, utility access, septic requirements where applicable, driveway access, drainage, and floodplain status. Rural or semi-rural properties can be attractive, but they may require more site preparation before a lender is comfortable.

A low land price can sometimes hide expensive work. For example, bringing utilities to the site, installing a septic system, improving access, clearing land, or correcting drainage can change the total budget. FHA approval is based on the whole property, not just the cost of the home.

If you want a smoother process, get site questions answered before ordering the home. A floor plan that works beautifully in one location may not be the right fit for a lot with setbacks, access limitations, utility challenges, or community restrictions.

Documents to gather before applying

Good documentation can save weeks. If you are using FHA financing for a manufactured home, ask your lender what they need before you are deep into the transaction. Requirements vary, but these are common items to prepare:

- Government-issued ID and Social Security number

- Recent pay stubs, W-2s, tax returns, or other income documents

- Bank statements and proof of funds for down payment and closing costs

- Purchase agreement or sales quote for the home

- Floor plan, model details, serial number, and manufacturer information

- HUD label numbers and data plate information, if available

- Texas Statement of Ownership for an existing home

- Land deed, survey, or lot lease information, depending on the purchase

- Foundation or installation documents, if the home is already placed

- Community approval documents, if the home will be in a manufactured home community

It is also smart to compare Loan Estimates from more than one lender. The Consumer Financial Protection Bureau explains how Loan Estimates help buyers compare interest rates, closing costs, and loan terms in a consistent format.

Common red flags that delay FHA approval

Some issues are fixable. Others can stop a deal completely. The earlier you spot them, the better.

The home was built before June 15, 1976

This is one of the clearest problems. FHA manufactured home financing generally focuses on HUD-code manufactured homes, not older true mobile homes. If the home predates the HUD Code, ask about other options before spending money on inspections or applications.

HUD tags or the data plate are missing

Missing documentation does not always mean the home is ineligible, but it can delay the file. If labels are painted over, removed, damaged, or unavailable, the lender may need third-party verification.

The foundation cannot be certified

An existing manufactured home may look stable, but still fail the foundation review. If the foundation does not meet required standards, repairs or upgrades may be needed before closing.

The title history is unclear

In Texas, ownership records need to match the transaction. If the Statement of Ownership, seller information, lien releases, or real property election is incomplete or inconsistent, the closing can slow down.

Additions were not permitted or appear unsafe

Unpermitted decks, enclosed rooms, attached structures, or roof modifications can raise questions. Lenders and appraisers may require repairs, permits, engineering review, or removal of unsafe work.

The lot is not ready

For land-and-home purchases, site readiness matters. Missing utilities, poor access, drainage concerns, floodplain complications, or zoning restrictions can create extra steps before the home can be approved and installed.

A practical FHA manufactured home buying process

A smoother FHA purchase usually starts before you fall in love with a specific home. Use this process to reduce surprises:

- Get pre-qualified with a lender that understands manufactured housing.

- Confirm whether you are pursuing FHA Title I, FHA Title II, or another loan type.

- Choose a HUD-code manufactured home that fits the lender’s requirements.

- Decide whether the home will be placed in a community or on private land.

- Verify title, Statement of Ownership, HUD labels, and data plate information early.

- Review foundation, installation, utility, and site requirements before closing.

- Leave room in your budget for taxes, insurance, lot rent if applicable, site work, and closing costs.

- Keep communication open between the retailer, lender, installer, community, and title professionals.

This may sound like a lot, but it is manageable when the right questions are asked in the right order.

How Homes2Go San Antonio helps buyers prepare

Homes2Go San Antonio works with buyers who want affordable, high-quality manufactured and mobile home options in the San Antonio area. If you are exploring FHA financing, the goal is to match your budget and lifestyle with a home and purchase path that make sense.

That can include comparing available home models, reviewing detailed floor plans, thinking through community versus private land placement, and connecting with trusted local lenders who understand manufactured home financing. For first-time buyers, that guidance can be especially valuable because FHA approval depends on more than choosing a home you like.

A manufactured home can be a smart path to homeownership, but only if the financing, property, and site all line up. Before you commit, ask about FHA eligibility, documentation, foundation expectations, and total monthly cost.

Frequently Asked Questions

Can FHA finance a used mobile home? FHA may finance an existing manufactured home if it meets HUD-code, title, foundation, appraisal, and lender requirements. A true mobile home built before June 15, 1976 is usually not eligible for standard FHA manufactured home financing.

Does FHA require a permanent foundation for a mobile home? For FHA Title II mortgage-style financing, a manufactured home typically must be permanently affixed to an acceptable foundation. Other loan structures may have different requirements, so confirm with your lender before choosing a home or site.

Can I use FHA for a manufactured home in a mobile home park? It depends on the loan program, lender, lease terms, and community approval. Mortgage-style FHA financing is often simpler when the home and land are treated as real property, while leased-lot purchases may require a different financing structure.

What happens if the HUD tag is missing? A missing HUD tag can delay the loan. Your lender may request verification from an approved record source such as IBTS. Do not assume the home is financeable until the lender confirms acceptable documentation.

Are FHA requirements different for single-wide and double-wide homes? Both single-wide and double-wide manufactured homes may be eligible if they meet FHA and lender standards. The home must still satisfy rules for HUD-code construction, size, condition, foundation, title, and site acceptability.

Ready to compare FHA-friendly manufactured home options in the San Antonio area? Contact Homes2Go San Antonio to explore available models, floor plans, financing paths, and community or land-home options that fit your homeownership goals.

Clayton Mobile Home Warranty: What’s Covered?

Clayton Mobile Home Warranty: What’s Covered? Manufactured Housing for Sale: How to Compare Smartly

Manufactured Housing for Sale: How to Compare Smartly

{kind=link}

{kind=link}

{kind=link}

{kind=link}