Buying a double wide is one of the most popular ways to get more space, a modern layout, and a predictable budget, especially in Texas where new manufactured homes can offer excellent value. But financing is where many buyers get stuck, because an FHA loan for double wide homes comes with very specific rules about eligibility, how the home is titled, and (most importantly) what counts as an acceptable foundation.

This guide breaks down the FHA pathways, the foundation standards lenders look for, and a practical set of steps to move from “shopping” to “clear to close.”

First, what counts as a “double wide” for FHA purposes?

“Double wide” is a common term for a multi section manufactured home (usually two sections) that is transported to the site and assembled. For FHA, the key is not the number of sections, it is whether the home is a HUD Code manufactured home.

In plain English, the home generally must:

- Be built on or after June 15, 1976 (when the HUD Code took effect)

- Have a HUD certification label (often called a HUD tag) on each section

- Have a data plate inside the home (typically in a kitchen cabinet, utility room, or closet)

Those labels and documents are essential during underwriting and appraisal.

For the official baseline standards, see HUD’s manufactured home program overview: HUD Manufactured Housing.

The two FHA options that can apply to a double wide: Title I vs Title II

Many buyers assume “FHA” is just one loan. With manufactured homes, you typically see two FHA structures:

- FHA Title I: often used when the home is financed more like personal property (commonly called chattel-style financing), sometimes used in land-lease communities

- FHA Title II: a traditional FHA mortgage structure, usually used when the home (and often the land) is treated as real estate

Here is a quick comparison to help you self-identify which path you are likely on.

| FHA option | Best for | What is being financed | Foundation expectations | Common sticking point |

|---|---|---|---|---|

| FHA Title I | Community placement or when land is not part of the loan | Home only, or home plus lot (varies) | Depends on lender and program, but installation still must meet HUD and local requirements | Fewer lenders offer it, program availability varies by area |

| FHA Title II | Land-home packages and private land scenarios | Typically home and land as real property | Permanent foundation meeting HUD guidelines is usually required | Title conversion to real property and foundation documentation |

HUD’s overview of the program categories is here: FHA Title I Manufactured Home Loan Program.

If you are shopping in San Antonio, the biggest practical difference is this: Title II is usually the easier story for underwriters to approve when the home is permanently affixed and treated as real estate, while Title I can be excellent when it is available and fits your placement plan.

FHA loan for double wide: core eligibility checklist

FHA guidelines are national, but each lender can add “overlays” (stricter rules). Expect the final answer to depend on the lender’s interpretation, your credit profile, and how the home is classified.

Borrower eligibility basics (typical FHA expectations)

Most FHA lenders will look for:

- Owner occupancy (FHA is generally for primary residences)

- A credit profile that meets FHA minimums, plus any lender overlays

- Verifiable income, employment, and acceptable debt-to-income ratios

- Sufficient funds for down payment, closing costs, and required reserves (if any)

FHA is known for allowing down payments as low as 3.5% with qualifying credit, but the exact minimum you can use can change with your credit score and lender overlays. If your down payment planning is tight, confirm the minimum required down payment with the specific lender before you pay for inspections or engineering.

Property eligibility basics (what the home must be)

For a double wide manufactured home to qualify, lenders commonly require:

- HUD Code compliance (post 6/15/1976), verified by labels/data plate

- The home is used as a residential dwelling and meets minimum property standards

- Proper installation consistent with HUD and local requirements

- For many Title II loans, the home must be treated as real property, not personal property

In Texas, the “real property vs personal property” part often comes down to titling and paperwork. Your lender and closing agent will tell you what is required for your exact scenario.

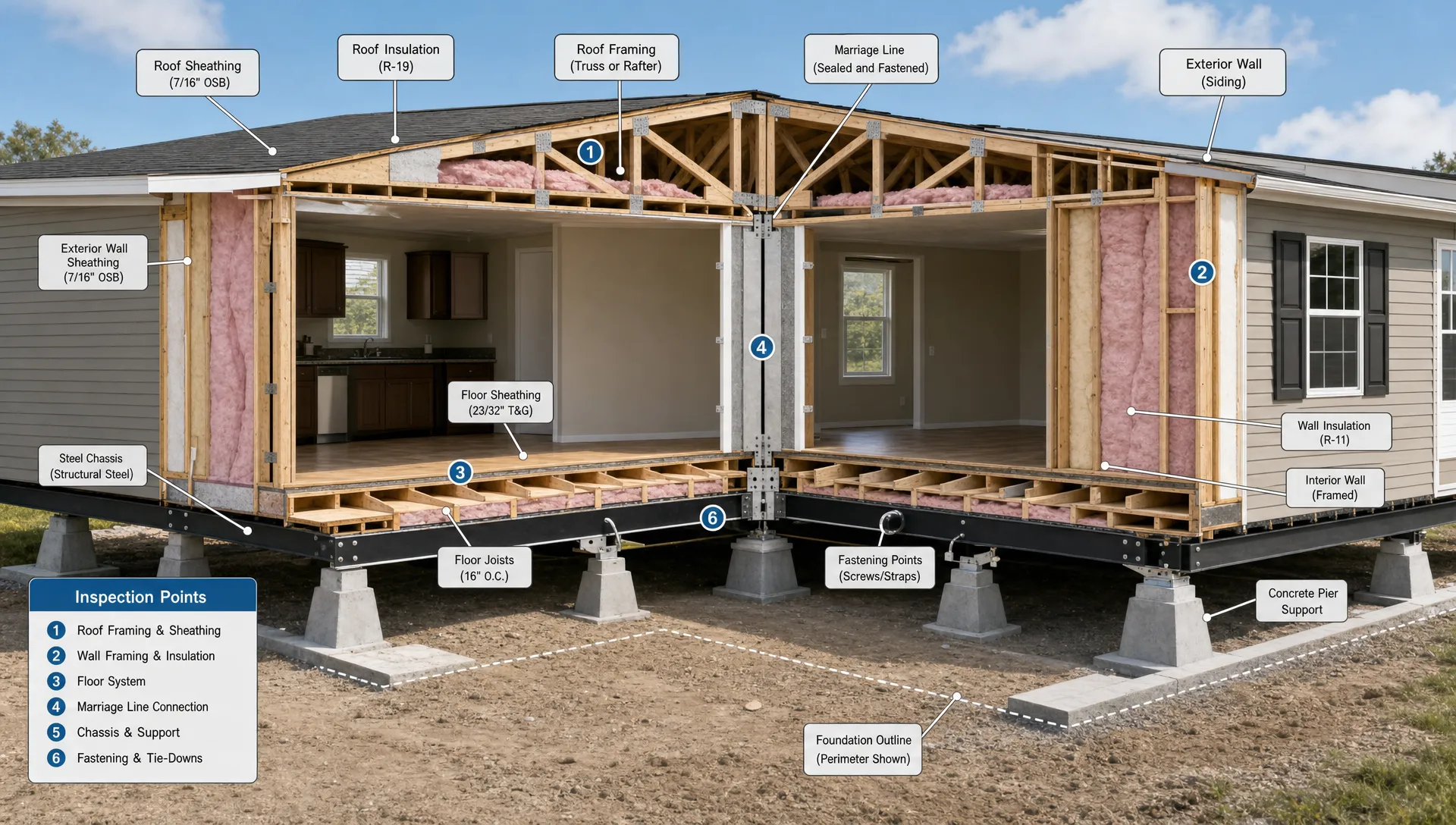

The foundation question: what FHA lenders usually mean by “permanent foundation”

If you hear “FHA needs a permanent foundation,” that is not just a concrete preference. The foundation is the bridge between “this is a moveable unit” and “this is real estate collateral.”

For many FHA Title II manufactured home mortgages, lenders typically want to see that the home:

- Is permanently affixed to an approved foundation system

- Is installed to resist wind, seismic, and other loads as required

- Has compliant anchoring and support

- Has utilities (water, sewer/septic, electric) installed in a code-compliant way

- Can be certified as meeting HUD’s permanent foundation guidance

A widely referenced standard is HUD’s Permanent Foundations Guide for Manufactured Housing (PFGMH), which engineers and lenders often use as the playbook for compliant designs.

Foundation types that are commonly acceptable (when designed correctly)

A double wide can potentially qualify with several foundation styles, as long as the design meets HUD guidance and local requirements:

- Concrete slab (with approved anchoring and load paths)

- Crawlspace (often with perimeter wall and engineered piers/footings)

- Basement foundation (less common, but possible if properly designed)

What usually does not work for a Title II mortgage is a setup that looks temporary or easily movable, or an installation missing documentation.

The document that makes or breaks approvals: engineer certification

A frequent friction point is not the foundation itself, it is proving it.

Many lenders require an engineer’s certification stating the foundation complies with HUD’s permanent foundation requirements (and/or applicable standards). If you are budgeting your project, include this line item early so it does not delay closing.

A simple “foundation readiness” table you can use while shopping

| Item to verify | Why it matters for FHA | Who usually provides it |

|---|---|---|

| HUD labels and data plate | Confirms HUD Code eligibility | Retailer, installer, homeowner documentation |

| Foundation design details | Shows it is engineered, not improvised | Installer or engineer |

| Anchoring/tie-down details | Demonstrates stability and compliance | Installer documentation |

| Engineer foundation certification (if required) | Common underwriting condition | Licensed professional engineer |

| Utility permits/approvals (as applicable) | Confirms code compliant installation | City/county, utility providers |

Step-by-step: how to get an FHA loan for a double wide without surprises

Below is a practical sequence that keeps most buyers out of the “we have to redo paperwork” loop.

- Decide where the home will go (land vs community): This choice affects whether you pursue an FHA Title II mortgage structure or explore Title I availability.

- Talk to an FHA lender early (before you pick a model): Ask specifically, “Do you finance manufactured homes as FHA, and what are your foundation and titling requirements for a double wide?”

- Get preapproved, not just prequalified: A full preapproval often catches income documentation issues and credit conditions earlier.

- Choose a double wide model that fits FHA and appraisal reality: Keep floor plan, size, features, and comparable sales in mind. Confirm HUD labels and documentation are available.

- Confirm the installation plan and foundation path in writing: Identify who is responsible for site work, foundation design, permits, and certifications.

- Lock down the land and site feasibility (if private land): Verify access, utilities, septic requirements, flood considerations, and any zoning or deed restrictions.

- Order appraisal and required inspections: Manufactured home appraisals can require specific comps and can take time, especially in more rural pockets outside San Antonio.

- Clear underwriting conditions: This is where engineer certification, title status, and documentation requests show up. Respond fast to avoid rate lock problems.

- Close and schedule installation milestones: Align delivery, setup, utility connections, and final inspections so the lender can release funds and the home can be occupied.

Common reasons FHA manufactured home deals get delayed (and how to prevent them)

Missing HUD labels or data plate

If the appraiser cannot verify HUD compliance, the loan can stall. Confirm documentation before you spend money on third-party services.

Foundation and installation documentation arrives late

Even when the foundation is fine, delays happen when the certification is not ordered early. Ask your lender up front whether an engineer letter is required.

Title classification confusion

Manufactured homes can be titled differently depending on whether the home is treated as personal property or real property. Your lender and closing agent should guide you, but you can reduce surprises by asking early, “What title status do you require at closing?”

Appraisal challenges

Some areas have fewer recent manufactured home sales, and that can complicate comparable selection. Picking a home with features common to the local market can help.

Practical planning tip: keep upgrade spending separate from loan-critical items

When buyers build a budget, they sometimes spend early on cosmetic upgrades and then get squeezed when the lender requests engineering, permits, or site changes.

If you want to personalize your interior after closing, consider planning those purchases after the loan is secure. Lighting is a good example because it can modernize a space quickly without changing the “loan critical” parts of installation. For inspiration, browse modern lighting options and save ideas for after you have keys in hand.

How Homes2Go San Antonio can help you line up the right FHA path

If you are buying in the San Antonio area, you rarely need “more options,” you need the right sequence and the right partners so financing, foundation, and placement stay aligned.

Homes2Go San Antonio can help you:

- Compare home models that fit your space and budget goals

- Coordinate documentation needed for lenders (floor plans, specs, and manufacturer info)

- Discuss financing routes, including FHA, based on whether you are placing on land or in a community

- Match you with trusted local lenders and guide you through the process

You can start with their financing overview here: manufactured home financing options.

Frequently Asked Questions

Can you get an FHA loan on a double wide in a mobile home park? Yes, it can be possible, but it depends on the FHA program type available through the lender and whether the lease and community requirements meet lender and FHA guidelines.

Does FHA require a permanent foundation for a double wide? For many FHA Title II manufactured home mortgages, lenders typically require the home to be permanently affixed to a compliant foundation and may require an engineer certification.

What is the difference between FHA Title I and Title II for a double wide? Title I is often used for manufactured homes in scenarios that resemble personal property financing (sometimes including communities), while Title II is closer to a traditional mortgage structure and commonly requires real property classification and a permanent foundation.

What documents should I confirm before I apply? At minimum, confirm the HUD certification labels and the data plate, and ask the lender what foundation and titling documents they will require to close.

Ready to see double wide models that can work with FHA financing?

If you are exploring an FHA loan for double wide options in San Antonio, the fastest way to avoid delays is to align three things early: the lender’s requirements, the installation and foundation plan, and the paperwork (HUD labels, title status, certifications).

Browse available homes and talk through financing with the Homes2Go San Antonio team at Homes2GoSA.com.

Rent to Own Trailer Home Near Me: Contract Traps to Avoid

Rent to Own Trailer Home Near Me: Contract Traps to Avoid Mobile Home Land Home Packages: What’s Included in Texas

Mobile Home Land Home Packages: What’s Included in Texas

{kind=link}

{kind=link}

{kind=link}

{kind=link}