Buying a manufactured home with an FHA loan can be a smart path to homeownership, but only if the home, the land (sometimes), and your paperwork meet FHA rules. The tricky part is that “FHA for manufactured homes” can mean two different programs with different qualifying requirements.

This guide breaks down what qualifies for an FHA loan and manufactured home purchase, what commonly disqualifies a property, and how to confirm eligibility before you spend money on inspections, appraisals, or moving plans.

FHA loan and manufactured home: Which FHA program are we talking about?

Most confusion comes from the fact that FHA-insured manufactured home financing typically falls into one of these buckets:

- FHA Title II (the “standard” FHA mortgage): Usually used when the manufactured home is permanently affixed and treated as real estate.

- FHA Title I (manufactured home loan program): Can be used for a manufactured home and may be used with or without land, depending on the structure of the loan and lender policies.

Here is a practical comparison to help you self-identify what you are shopping for.

| Item | FHA Title II (FHA mortgage) | FHA Title I (manufactured home program) |

|---|---|---|

| Typical use case | Land + home financed together as real property | Home-only financing, or home + lot, often when not set up as real estate |

| Foundation requirement | Permanent foundation is generally required | Requirements vary by lender and loan structure, foundation standards still matter |

| Land ownership | Commonly required (home is real property) | Can be structured without owning the land in some cases |

| Property type | Primary residence | Primary residence |

| Who sets many details | FHA + lender + appraiser | FHA + lender (program is less common, lender overlays are common) |

For official program overviews, HUD is the most reliable starting point for both FHA-insured mortgages and the FHA Title I program.

What qualifies on the home itself (HUD code, tags, and condition)

No matter which FHA path you use, the home must meet baseline standards that prove it is a compliant manufactured home and safe to finance.

1) It must be a HUD Code manufactured home (not a pre-1976 “mobile home”)

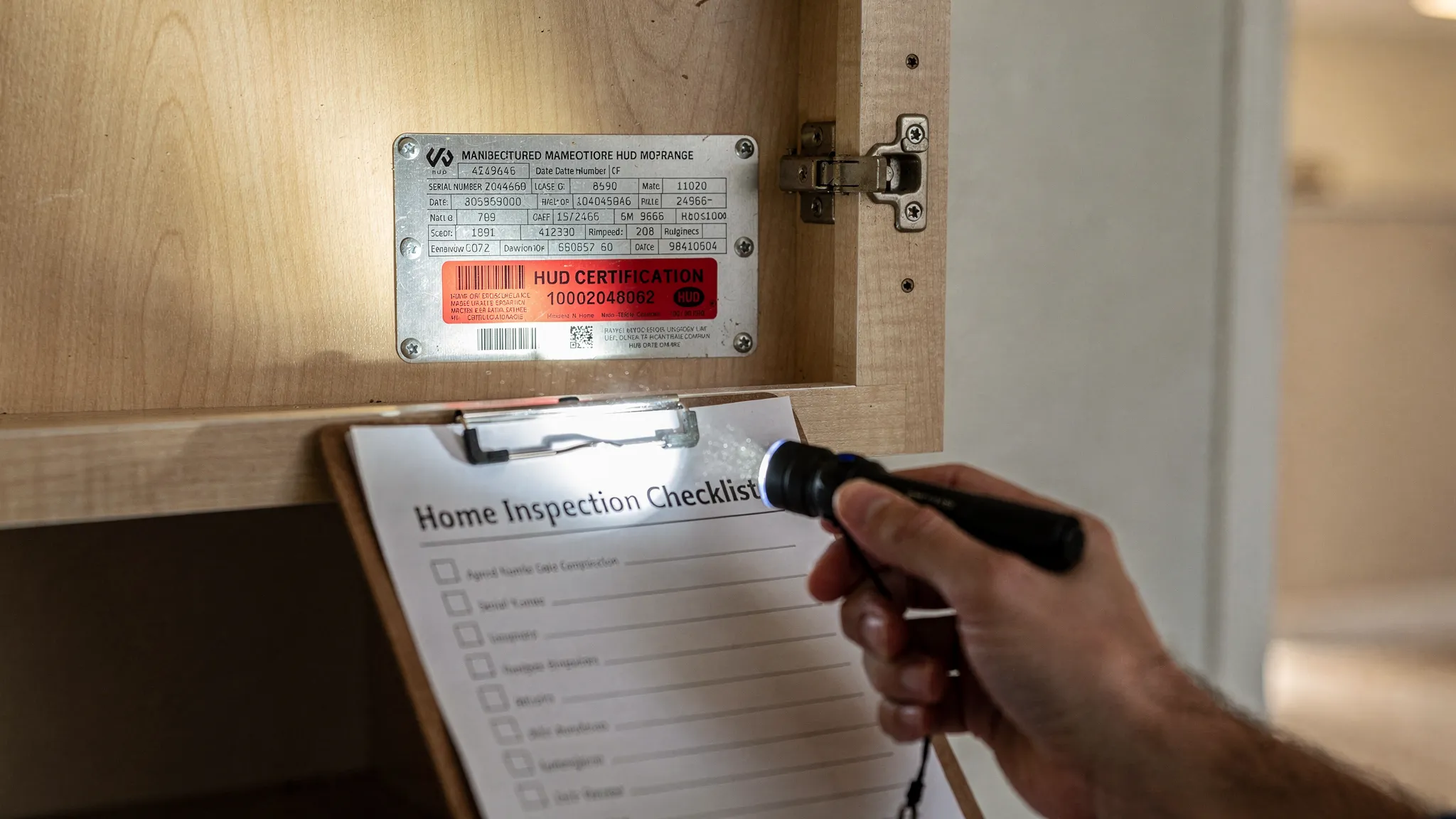

In FHA conversations, “manufactured home” usually means a home built to the HUD Manufactured Home Construction and Safety Standards (the HUD Code), which began in 1976. Practically, buyers and lenders verify this with:

- HUD certification labels (HUD tags) affixed to each transportable section

- A data plate (often inside a cabinet door, utility closet, or electrical panel area) listing key build information

If a home is older than the HUD Code, or if it cannot be verified as HUD Code compliant, it often becomes very difficult to finance with FHA.

2) The home must be in livable, financeable condition

FHA loans require the home to be safe, sound, and sanitary. During the FHA appraisal process, issues that commonly create problems include:

- Non-functioning utilities, missing heat source, or unsafe electrical

- Active roof leaks or significant water intrusion

- Structural concerns (unresolved settling, obvious frame or pier failures)

- Health and safety hazards that an appraiser flags for repair

For manufactured homes, FHA appraisers and lenders also pay close attention to whether the home appears properly installed and maintained.

3) Size, layout, and use must fit “primary residence” lending

FHA is intended for owner-occupants. In most cases, you should expect requirements such as:

- You will live in the home as your primary residence

- The property type fits typical residential lending standards (your lender and appraiser will confirm)

If you are looking for an investment-only property, FHA is usually not the right tool.

Foundation and installation: The make-or-break factor for FHA Title II

If you are pursuing an FHA Title II mortgage (the most common “FHA loan” people mean), the foundation question often determines whether the home qualifies.

Permanent foundation requirements

For Title II financing, the home generally needs to be:

- Permanently affixed to a foundation that meets FHA and HUD standards

- Installed in a way that supports long-term durability (anchoring, piers, footings, and site conditions all matter)

Many lenders will require a foundation certification from a qualified engineer to confirm the foundation complies with FHA/HUD requirements.

A key reference used across the industry is HUD’s Permanent Foundations Guide for Manufactured Housing (often cited in underwriting and engineering reviews). You can find it via HUD user resources here: Permanent Foundations Guide for Manufactured Housing (PDF).

Why this matters in Texas and around San Antonio

Soil conditions, drainage, and site prep are not small details in South Texas. Even when a home looks “set,” the lender still needs documentation that the installation is compliant.

If you are comparing private land vs a land-lease community, keep in mind:

- Title II usually fits more cleanly when the home is real property on owned land.

- Title I may be a better conversation starter when the home is not being titled as real property.

If you are still deciding between land options, Homes2Go San Antonio’s guide on land and home packages in San Antonio gives a helpful overview of how land, utilities, permits, and financing intersect.

Land and title: What qualifies as “real estate” for an FHA mortgage?

For FHA Title II, the home is typically financed like a house, meaning it must be treated as real property (real estate), not just personal property.

Real property vs personal property (why lenders care)

- Personal property is closer to how a vehicle is titled, common with some manufactured homes, especially in land-lease communities.

- Real property means the home is legally tied to land and recorded like a traditional home.

To qualify for Title II in many cases, the home needs to be:

- On a permanent foundation

- On land that you own (or are buying)

- Properly titled/recorded as real property according to state and local rules

Texas paperwork considerations (high level)

Texas has specific processes for manufactured home ownership and location documentation. Buyers commonly encounter the Statement of Ownership and Location (SOL) process administered through the Texas Department of Housing and Community Affairs (TDHCA). Your lender and closing company typically guide what must be filed and recorded for your loan type.

Because title and classification details can vary by property and county, confirm early with your lender what they will require to treat the home as real property.

Borrower qualification basics (what FHA looks for)

Even if the home qualifies, you still have to qualify. FHA guidelines are designed to be flexible, but lenders can add overlays.

Down payment and credit

Many buyers choose FHA because it can allow a lower down payment than some conventional options. Common baseline rules you will hear quoted are:

- 3.5% minimum down payment with 580+ credit score (typical FHA guideline)

- 10% down if credit scores are lower (guideline-based, lender overlays apply)

Your lender will confirm what applies to your exact profile.

Income, debt-to-income ratio, and documentation

Expect your lender to review:

- Stable, documentable income (W-2, 1099, retirement, etc.)

- Your monthly debts and projected housing payment

- Credit history and any recent derogatory events

FHA can be more forgiving than some loan types, but the home type (manufactured) can cause lenders to be more conservative. Pre-approval before shopping is especially valuable.

Mortgage insurance (part of the FHA cost)

FHA loans include mortgage insurance (upfront and annual components, depending on the loan). This affects your monthly payment and long-term cost comparison versus other loans.

If you are weighing multiple financing types, the broader overview in Mobile Homes San Antonio: A Quick Buyer Guide can help you compare FHA with chattel, conventional, and other options at a high level.

What commonly disqualifies a manufactured home for FHA

This is where buyers can save time and money by screening early.

Missing HUD tags or data plate

If the HUD certification labels are missing, damaged, or cannot be verified, lenders may not be able to confirm the home is HUD Code compliant.

Tip: Ask for clear photos of the HUD tags and data plate before you commit to a specific home.

Not on a permanent foundation (for Title II)

A manufactured home that is not permanently installed to FHA/HUD standards can fail underwriting for Title II, even if it is otherwise in great condition.

Title and classification issues

Common snags include:

- Unreleased liens

- Ownership not clearly documented

- The home not being eligible to convert to (or be recorded as) real property for a Title II mortgage

Prior movement history (lender policy can matter)

Some lenders are cautious about manufactured homes that have been moved from their original installation site, especially for FHA mortgages on existing (not brand-new) homes. Policies vary, so ask your lender early if movement history affects eligibility.

Appraisal problems specific to manufactured homes

Even when a home “qualifies,” an FHA appraisal can create friction if:

- Comparable sales are limited

- The home has unpermitted additions or questionable modifications

- Condition items trigger required repairs

How to confirm a specific home qualifies before you apply

A quick qualification check can prevent weeks of back-and-forth later.

Ask for these items up front

- Photos of HUD tags and the data plate

- The home’s make, model, year, and serial/VIN information (as shown on documents)

- Foundation information (if already installed), including any engineering letters/certifications

- A clear understanding of whether the deal is home-only, land-home, or community placement

Align the home with the right loan structure

If your goal is an FHA Title II mortgage, ask your lender (before appraisal) how they want the home structured:

- Will it be financed as real property?

- Do they require an engineer’s foundation certification?

- Do they require the home to be on owned land?

If you are still in the shopping phase, it can help to tour homes with financing in mind. Homes2Go San Antonio notes they offer expert guidance and flexible financing options, which can be useful when you are matching a home model and placement to lender requirements. You can start exploring options at Homes2Go San Antonio.

San Antonio buyer tips: Choosing a home that is easier to FHA-finance

A few practical choices can reduce financing friction:

Prefer homes with complete documentation

In manufactured housing, clean paperwork is a feature. Homes that have verifiable HUD labels, clear ownership history, and documented installation are typically smoother to finance.

Consider energy-efficient models, but keep financing fundamentals first

Energy efficiency can lower operating costs, which helps affordability, but it does not replace core FHA qualification requirements like HUD Code compliance and foundation standards. If you want a shopping checklist for performance features in Texas heat, see Energy Efficient Manufactured Homes: Save More in Texas Heat.

Budget for third-party requirements

Even a “perfect” FHA scenario often includes third-party items such as:

- Appraisal

- Title work and recording

- Foundation certification (common for Title II manufactured home loans)

- Insurance (and flood insurance if required)

For flood risk questions, lenders and insurers commonly reference FEMA flood maps and determinations. FEMA’s map service center is available here: FEMA Flood Map Service Center.

A simple checklist: What qualifies for an FHA loan and manufactured home purchase?

Use this as a quick screen while you shop.

| Category | Typically needed for FHA eligibility | What to verify early |

|---|---|---|

| HUD Code compliance | Built to HUD Code (generally post-1976) | HUD tags and data plate are present and readable |

| Property condition | Safe, sound, sanitary | Roof, utilities, electrical, plumbing, no major hazards |

| Foundation (Title II) | Permanent foundation per FHA/HUD standards | Installation details, engineering certification if required |

| Title and legal status | Clear ownership and lien status | SOL/title documents, liens released, correct names/serials |

| Land (Title II) | Usually owned land and treated as real property | How the home will be classified and recorded |

| Occupancy | Primary residence | You plan to live there full-time |

Next step: Get loan clarity before you pick a floor plan

A manufactured home can absolutely qualify for FHA financing, but the safest approach is to confirm the loan type first (Title I vs Title II), then shop only homes that match that lane.

If you are buying in the San Antonio area and want help aligning the home, placement, and financing path, Homes2Go San Antonio can help you compare models, review floor plans, and connect with trusted local lenders. Start here: Homes2Go San Antonio.

How to Find FHA Mobile Home Lenders in Texas

How to Find FHA Mobile Home Lenders in Texas Affordable Housing Options in San Antonio: 2026 Guide

Affordable Housing Options in San Antonio: 2026 Guide

{kind=link}

{kind=link}

{kind=link}

{kind=link}