Financing is often the hardest part of buying a manufactured home, not the shopping. The reason is simple: not every FHA-approved lender actually offers FHA loans for manufactured homes, and the rules differ depending on whether you’re financing the home only or the home plus land.

This guide breaks down how FHA manufactured home loans work and gives you a practical process to find FHA mobile home lenders in Texas, vet them quickly, and avoid the most common “we can’t finance that home” surprises.

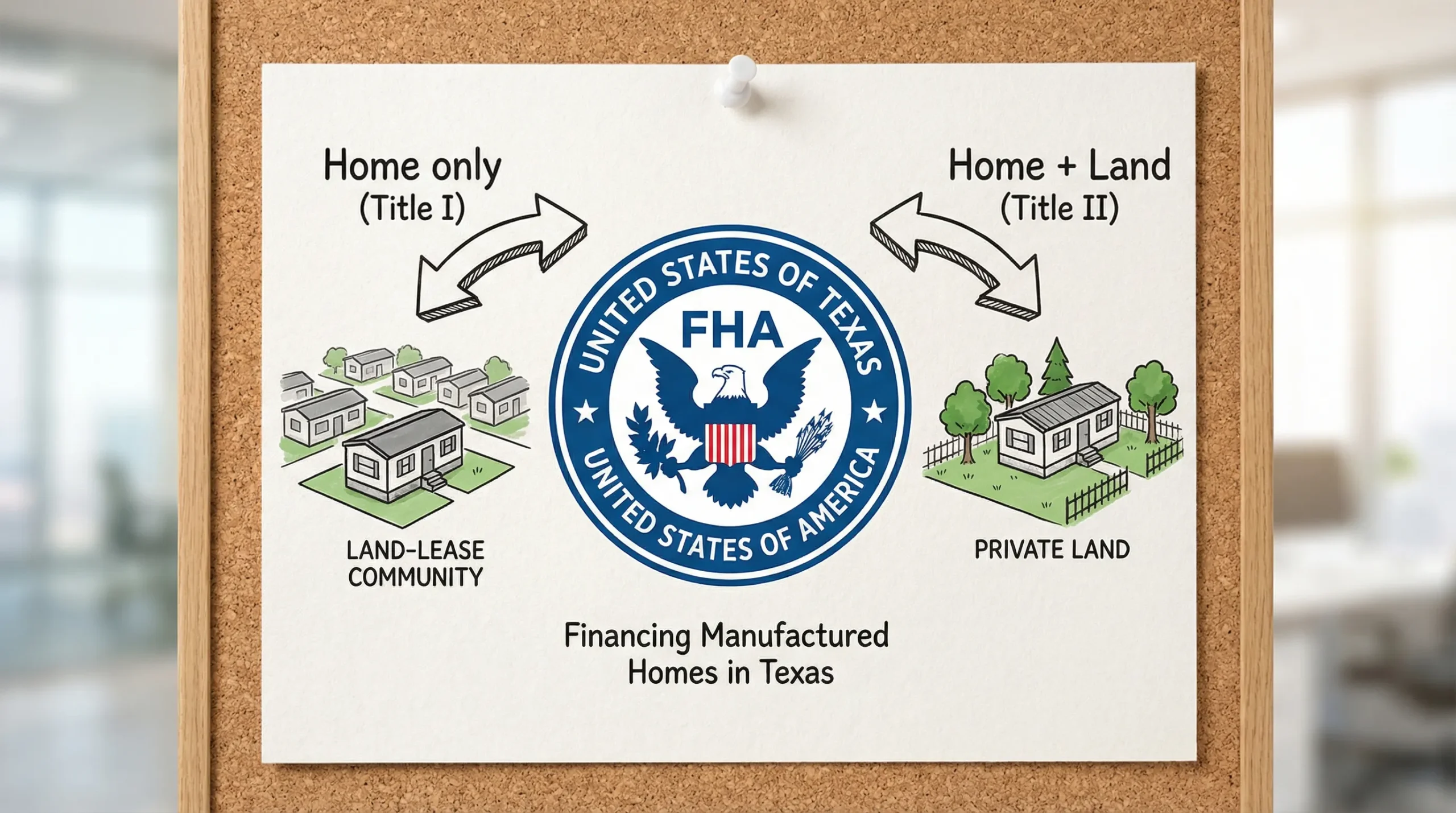

First, know what FHA will and will not finance

Many buyers use the phrase “mobile home,” but FHA financing usually centers on manufactured homes built to the federal HUD Code (generally homes built on or after June 15, 1976). If a home is older (a true pre-1976 mobile home), it is much harder to finance through standard FHA programs.

At a high level, FHA insures two different paths that people commonly use for manufactured housing:

- FHA Title I: often used for home-only financing (personal property), and sometimes for a lot.

- FHA Title II: used for home plus land as real estate (a more traditional mortgage structure).

Here’s a simplified comparison to help you orient your lender search.

| FHA option | What it’s commonly used for | Best fit if you… | Key “gotchas” to expect |

|---|---|---|---|

| FHA Title I (manufactured home) | Home-only financing (often treated as personal property), sometimes home + lot | Want to place a home in a land-lease community, or you are not buying land right now | Fewer lenders offer it, and terms/fees can vary a lot by lender |

| FHA Title II (manufactured home mortgage) | Home + land financed together as real estate | Are buying land, already own land, or want a land-home package | Typically requires the home to meet real-property and foundation requirements, plus appraisal rules |

For official program overviews, start with HUD’s manufactured housing and FHA resources and then confirm details with the lender you’re considering.

- HUD (search “FHA manufactured home Title I” and “Title II manufactured home” on HUD for current guidance)

- FHA mortgage limits lookup by county

Decide which FHA route you need before you call lenders

You will save a lot of time (and avoid getting bounced between call centers) if you can answer one question upfront:

Are you financing the home alone, or the home and land together?

If you need “home-only” financing

This is common when you:

- plan to live in a manufactured home community (lot rent)

- already have a pad/space secured

- want a lower upfront cost and do not want to purchase land yet

In this scenario, you’ll specifically ask lenders whether they offer FHA Title I manufactured home loans (not just “FHA loans”).

If you need “home + land” financing

This is common when you:

- are buying land in Texas

- already own land and want to place a home on it

- are pursuing a land and home package

Here you’re looking for lenders who offer FHA Title II financing for manufactured homes, and who are comfortable with manufactured home appraisals and foundation requirements.

If you’re still deciding between private land and a community, our local guides can help:

- Mobile homes in San Antonio: a quick buyer guide

- Land and home packages in San Antonio: complete guide

Where to find FHA mobile home lenders in Texas (the most reliable methods)

Because manufactured home FHA lending is specialized, your goal is to find lenders in the overlap of:

- FHA-approved lenders, and 2) lenders who actively do manufactured housing loans.

1) Use HUD tools to build a starting lender list

A smart first step is to use HUD’s lender resources to find FHA-approved lenders operating in Texas, then call and confirm they do manufactured home FHA loans.

What to do:

- Use HUD’s lender search resources on HUD.gov (look for the FHA lender list pages).

- Filter by Texas, then create a shortlist.

- Call and ask one direct question: “Do you offer FHA loans for manufactured homes, and do you do Title I, Title II, or both?”

Important: many lenders are FHA-approved but will still say “no” to manufactured homes, or will only do them in limited cases.

2) Contact manufactured-home experienced mortgage brokers (Texas-based)

A broker can be valuable if you’re hitting dead ends. The key is to choose someone who explicitly mentions manufactured housing experience and can explain the difference between Title I and Title II.

When you speak to a broker, ask how many manufactured home FHA closings they’ve completed recently in Texas, and what stopped deals they’ve seen (missing HUD labels, title issues, foundation problems, and so on).

3) Ask local credit unions and community banks the right way

Some Texas credit unions and community banks are more flexible than large national lenders, but you need to use precise language.

Instead of asking “Do you do FHA?”, ask:

- “Do you do FHA Title II loans for manufactured homes on owned land?”

- “Do you do FHA Title I manufactured home loans (home-only)?”

- “Do you require the home to be new, or will you finance a used manufactured home that meets HUD Code and appraisal requirements?”

4) Use your retailer and community to find lender matches

Manufactured home retailers and communities often know which lenders are actively lending right now, and which ones understand the documentation needed.

At Homes2Go San Antonio, we can guide you through model selection and help you connect with trusted local lenders that are familiar with manufactured homes (without you having to cold-call dozens of banks).

You can start browsing options here: Homes2Go San Antonio.

How to vet a lender quickly (and avoid wasted applications)

Once you’ve found potential FHA mobile home lenders in Texas, you want to vet them before a hard credit pull and before you pay for an appraisal.

Here are the highest-impact questions.

| Question to ask the lender | Why it matters | What a good answer sounds like |

|---|---|---|

| “Do you offer FHA for manufactured homes, and is it Title I, Title II, or both?” | Confirms they truly do manufactured home FHA lending | “Yes, we do Title II on owned land, and we can discuss Title I if you’re in a community.” |

| “Will you finance a home in a land-lease community?” | Not all programs or lenders allow the same scenarios | Clear criteria (lease terms, community requirements) |

| “Do you require the home to be on a permanent foundation (Title II)?” | Foundation and classification can make or break approval | They explain foundation expectations and documentation |

| “What credit score and debt-to-income rules do you use for manufactured homes?” | Many lenders have overlays beyond FHA minimums | They’re transparent about their overlays |

| “Do you have appraisers who routinely handle manufactured homes in my county?” | Appraisal issues are a common delay | “Yes, we have a panel familiar with manufactured comps.” |

| “What home documentation will you need?” | Prevents last-minute surprises | They mention HUD data plate/labels, purchase contract, and title/ownership docs |

Red flags that usually mean “keep looking”

A lender may not be the right fit if they:

- can’t clearly explain Title I vs Title II

- say “We do FHA” but dodge the phrase “manufactured home”

- have no plan for manufactured home appraisals in your area

- require conditions that don’t match your plan (example: you want a community placement, but they only do land-home)

Prepare these documents to move faster

Manufactured home financing can involve extra steps compared to a site-built home, so being organized helps.

Bring these items to your lender conversation (or have them ready to upload):

- Government-issued ID and Social Security number (or equivalent documentation for the application)

- Recent pay stubs, W-2s (or 1099s), and tax returns if requested

- Recent bank statements (and documentation for large deposits)

- A purchase agreement or quote for the home you’re buying

- The home’s details and documentation (model, year, size, serial/VIN info, and HUD tags/data plate details when applicable)

- If you own land: proof of ownership, and any available survey or legal description

- If you’re placing on land: any known site details (utilities, septic/well, flood zone info if applicable)

Tip: if you’re comparing homes, keep copies of floor plans and specs handy. Lenders and appraisers often ask for them.

Common Texas issues that can block FHA manufactured home financing

Texas is a strong market for manufactured housing, but a few local realities can slow down an FHA loan if you aren’t ready for them.

1) Title and ownership paperwork for the home

Manufactured homes can be titled differently than site-built homes. Depending on the transaction, you may need state-issued ownership documentation and updates to match the buyer, location, and lienholder.

For Texas-specific guidance, review resources from the Texas Department of Housing and Community Affairs (TDHCA) and confirm lender requirements for your exact scenario.

2) Classification: personal property vs real property

If you’re doing Title II (home + land), the lender usually wants the home treated as real estate with the correct documentation and a compliant foundation setup. If you’re doing Title I, the structure can differ.

The practical takeaway: tell the lender early whether you’re buying land, already own land, or plan to be in a community.

3) Appraisal comps and local market fit

Manufactured home appraisals can be delayed if there are limited comparable sales nearby, especially for unique homes or rural placements.

You can reduce surprises by:

- choosing a home style common in your area

- working with a lender who routinely appraises manufactured homes in your county

- ensuring the home site and installation plan match lender expectations

4) Property condition and “unfinanceable” homes

Not every manufactured home is financeable under FHA. Common issues include missing HUD labels/data plates, major unpermitted additions, or older pre-HUD-code units.

If you’re shopping used homes, ask upfront what documentation exists and whether the home was moved, modified, or repaired.

A simple workflow to find the right lender match

If you want a repeatable process (instead of random Google searches), use this:

Step 1: Define your scenario

Write down:

- home-only or home + land

- city/county in Texas

- community placement or private land

- new or used home

Step 2: Build a shortlist of 5 to 10 lenders

Pull from:

- HUD lender resources (HUD.gov)

- local brokers with manufactured home experience

- local banks and credit unions

- referrals through your retailer and communities

Step 3: Run the “Title I/Title II” phone screen

Ask the six questions in the vetting table above. Eliminate anyone who can’t answer clearly.

Step 4: Get prequalified, then shop homes confidently

With prequalification in hand, you can focus on the right price range and home specs, and move faster when you find the model you want.

How Homes2Go San Antonio can help

If you’re buying in the San Antonio area, Homes2Go San Antonio can help you match your home choice to financing realities. That includes:

- touring a wide selection of manufactured and mobile home models

- reviewing floor plans and specs (so you know what lenders will ask for)

- guidance through the buying process, especially for first-time buyers

- connecting you with trusted local lenders and financing paths that fit your plan

Explore available homes and get guidance here: Homes2Go San Antonio.

Frequently Asked Questions

Are FHA loans available for mobile homes in Texas? Yes, in many cases, but it typically applies to HUD-code manufactured homes and depends on whether you’re financing the home only (often Title I) or the home plus land (Title II). Not every FHA lender offers manufactured home financing.

What’s the difference between FHA Title I and Title II for manufactured homes? Title I is commonly used for home-only financing (and sometimes a lot), while Title II is a mortgage-style loan for home plus land as real estate. Eligibility and documentation requirements are different.

Can I use FHA financing if I’m putting the home in a mobile home park? Sometimes, but it depends on the lender and the program structure. Many buyers in communities look at home-only options, so you’ll want to ask lenders specifically about community placements.

Do FHA manufactured home loans require a permanent foundation? Often yes for Title II (home + land mortgages), along with other real-property and appraisal requirements. Requirements vary by lender overlays and the specific transaction.

What credit score do I need for an FHA manufactured home loan? FHA has general minimum guidelines, but manufactured home lenders often apply stricter overlays. The fastest way to know is to ask each lender their minimum score and debt-to-income requirements for manufactured homes.

How do I confirm a lender is truly an FHA mobile home lender in Texas? Start with FHA-approved status (via HUD resources), then verify they actively originate manufactured home FHA loans by asking whether they offer Title I, Title II, or both, and whether they’ve closed similar loans in your county recently.

Talk with a local team that can connect you to the right lenders

If you want help narrowing down FHA mobile home lenders (and choosing a home that fits lender requirements), Homes2Go San Antonio can walk you through the process and connect you with trusted local financing options.

Get started here: Homes2Go San Antonio.

FHA Financing for Mobile Homes: What’s Covered

FHA Financing for Mobile Homes: What’s Covered FHA Loan and Manufactured Home: What Qualifies

FHA Loan and Manufactured Home: What Qualifies

{kind=link}

{kind=link}

{kind=link}

{kind=link}