Buying a manufactured home can be one of the fastest paths to homeownership in San Antonio, but the financing can feel confusing, especially when people say “mobile home” and “FHA loan” in the same sentence.

The good news is that FHA financing can work for manufactured homes, and in some cases it can be a strong option for buyers who want a lower down payment and more flexible credit guidelines than many conventional programs. The catch is that FHA has very specific rules about the home itself, how it is installed, and how the property is titled.

This guide breaks down FHA loans for mobile homes in San Antonio in plain English, including the difference between FHA Title I and Title II, what typically disqualifies a home, and how to set your purchase up for approval.

Can you use an FHA loan for a “mobile home” in San Antonio?

In most San Antonio home searches, “mobile home” is used as shorthand. For financing, what matters is whether the home is a HUD-code manufactured home.

- Manufactured home (HUD code): Built in a factory to federal HUD standards. Generally eligible for FHA if it meets program rules.

- True “mobile home” (pre-1976): Built before June 15, 1976 (before modern HUD standards). Often not eligible for FHA financing.

If you are not sure what you are looking at, check the home for:

- A HUD certification label (metal tag on the exterior of each section)

- A data plate (often inside a cabinet door, closet, or electrical panel area)

For program overviews directly from the source, see HUD’s pages on the FHA-insured manufactured home loan program (Title I) and FHA home loans.

FHA Title I vs. FHA Title II: the most important choice

When buyers say “FHA loan,” they may mean one of two different programs for manufactured housing:

- FHA Title I: Can be used for a manufactured home with or without land (structure only, lot, or both), depending on the deal structure and lender.

- FHA Title II: A traditional FHA mortgage used when the manufactured home is treated like real estate (home plus land), typically on a permanent foundation.

Here is the practical difference:

| Feature | FHA Title I (Manufactured Home Loan) | FHA Title II (FHA Mortgage) |

|---|---|---|

| What it can finance | Home only, lot only, or home + lot (varies by lender) | Typically home + land together |

| Common setup in San Antonio | Home placed in a land-lease community, or home-only purchase | Land-and-home package or owned land |

| How the home is titled | Often personal property (chattel), depending on structure | Must be real property in most cases |

| Foundation expectations | Installation must meet standards, permanent foundation not always required | Permanent foundation is generally required |

| Down payment | Varies by lender and structure | Often as low as 3.5% (if borrower qualifies) |

If you are deciding between the two, the quickest rule of thumb is:

- Choose Title II if you want the most “mortgage-like” FHA experience and you will own the land.

- Explore Title I if you are buying the home with a different structure (for example, home-only) or placing it in a community where the land is leased.

Homes2Go San Antonio summarizes these options on its manufactured home financing page, including FHA paths alongside other loan types.

FHA rules that most often affect manufactured home approvals

FHA approval is usually less about your dream floor plan and more about whether the deal checks several non-negotiable boxes.

1) The home must qualify as a HUD-code manufactured home

FHA financing is built around HUD-code homes (post-1976). If a seller cannot verify HUD labels/data plate information, lenders may not proceed, even if the home looks “new enough.”

Tip: When shopping, ask early for the HUD label numbers and confirm the home’s build date.

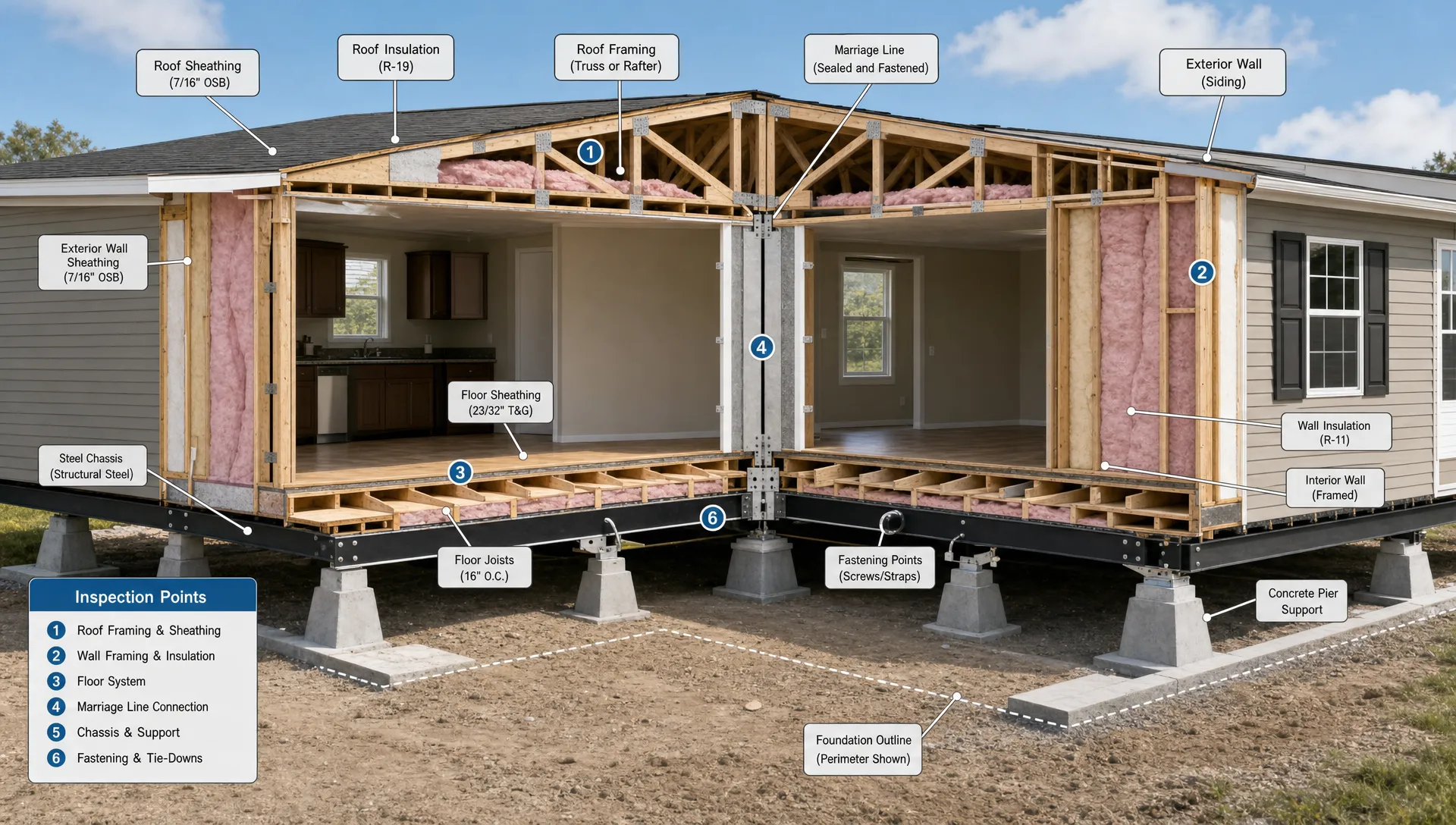

2) The property must meet FHA’s expectations for safety and habitability

FHA loans require an appraisal, and the appraisal is not just about value. It also checks for basic health and safety conditions.

Common manufactured-home issues that can trigger repairs or denial include:

- Damaged roofing, siding, skirting, stairs, or handrails

- Electrical or plumbing defects

- Evidence of moisture intrusion or soft flooring

- Missing smoke and carbon monoxide alarms (requirements vary)

3) Title II usually requires the home to be real property (not just personal property)

For FHA Title II financing, the home generally needs to be treated like real estate, which usually means:

- Installed to code on an acceptable foundation system

- Properly recorded or titled as real property (process varies by state and county)

This is one of the biggest reasons a manufactured-home FHA deal can stall. A home can be beautiful and still fail the “real property” requirement if it is not classified correctly.

4) Land and lease structure matter (especially in communities)

If you are placing the home in a manufactured home community, the lease terms can matter a lot for lender approval, particularly under Title I structures.

Before you choose a community, confirm:

- Minimum lease term requirements the lender expects

- Rules about subleasing, home removal, and resale

- Utility responsibility (owner vs community)

Homes2Go can also help buyers compare community options, including what to look for in approvals, lot rent, and fees. (If you are evaluating parks, their roundup of mobile home parks in San Antonio is a helpful companion.)

5) Borrower qualifications still apply, even if the home is affordable

FHA is known for accessibility, but it is not automatic approval. Lenders will still evaluate:

- Credit history and recent late payments

- Debt-to-income ratio

- Stable income and employment documentation

- Cash to close and reserves (depending on file strength)

If you are early in the process, it often helps to get a lender conversation started before you pick a home, so you can shop within the loan structure you actually qualify for.

San Antonio-specific factors that can impact an FHA manufactured home loan

Even with the right loan program, local realities can affect timing and approval.

Floodplain and drainage risk

Some San Antonio and Bexar County areas have higher flood exposure than buyers expect, especially near creeks and low-lying tracts. Flood zone status can affect:

- Insurance requirements

- Appraisal conditions

- Total monthly payment qualification

You can check a property’s flood risk using FEMA’s official tools like the FEMA Flood Map Service Center.

Utilities and site readiness on private land

If you are buying land (or already own it), lenders and appraisers will pay attention to whether the homesite supports normal, year-round living, including:

- Legal access

- Water/sewer or septic feasibility

- Electric service availability

This is where many buyers underestimate total project complexity. A land-and-home approach can still be smooth, but you want the plan clear before underwriting.

If you are considering this route, see Homes2Go’s guide to land and home packages in San Antonio for the typical sequence and the major cost categories.

Insurance in a hail, wind, and heat reality

Texas weather is a real underwriting factor. Expect the lender to require homeowners insurance that meets coverage guidelines. In some areas, wind or hail deductibles can be significant, which changes your monthly affordability.

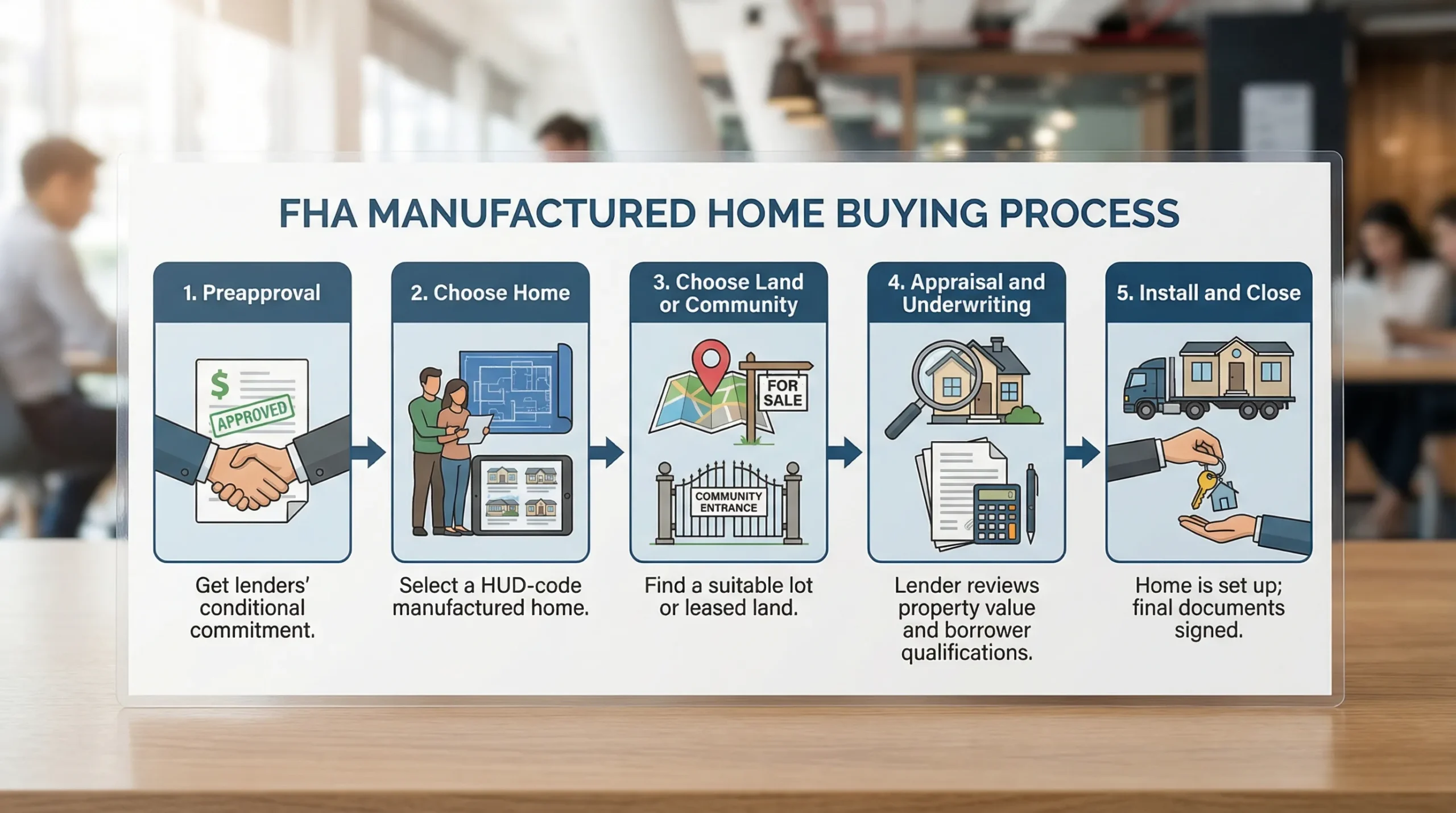

What the FHA manufactured home process usually looks like

FHA timelines vary by lender and property type, but most successful purchases follow a similar path.

Start with the loan structure, not the floor plan

Before you fall in love with a home, confirm which structure you are pursuing:

- Title I home-only or home + lot

- Title II land-and-home mortgage

This decision affects what homes and placements are eligible, and it determines what documentation you will need.

Get a lender preapproval that is specific to manufactured homes

Not every lender who “does FHA” wants manufactured homes. Ask directly if they do:

- FHA Title I manufactured home loans

- FHA Title II mortgages for manufactured homes

Also ask what installation, foundation, and titling standards they require, because lender overlays are common.

Match the home and the site to FHA requirements

This is where experienced guidance saves time. You typically want to validate:

- HUD labels and data plate information

- Installation plan (especially for Title II)

- Whether the land or community lease will satisfy the loan

Appraisal, underwriting, and closing

Manufactured home transactions can involve more “moving parts” than site-built homes, especially if installation and inspections are happening around the same time as the loan process.

To reduce surprises, gather documentation early:

- Income documents (pay stubs, W-2s, tax returns if needed)

- ID and residency documents

- Bank statements for down payment and closing costs

- Home documentation (serial/label numbers, specs, seller docs)

Common FHA manufactured home deal-breakers (and how to avoid them)

These problems are avoidable if you plan for them early:

- The home is pre-1976: Confirm build date and HUD labels before negotiating.

- The home cannot be properly classified for the loan type: Align your plan (Title I vs Title II) with titling and foundation reality.

- The community lease does not meet lender requirements: Review lease terms with the lender before you commit.

- Site work and utilities were underestimated: Budget and timeline issues can derail underwriting.

- The appraiser cannot find good comparable sales: This is not uncommon with certain models or areas. A lender experienced in manufactured homes can help set expectations.

How Homes2Go San Antonio can help

FHA loans for mobile homes in San Antonio are doable, but they are detail-driven. A big part of success is choosing a home and placement that match the financing path from day one.

Homes2Go San Antonio can support you by:

- Showing a wide selection of manufactured home models with detailed floor plans

- Providing expert guidance on the buying and setup process

- Connecting you with trusted local lenders, including FHA pathways where appropriate

- Helping you explore home communities or land-and-home options

If you want to explore FHA-friendly options and compare financing paths for your budget, start with their financing options page or browse their educational buyer resources like the mobile home buyer guide for San Antonio.

Manufactured Homes for Sale: San Antonio Market Guide

Manufactured Homes for Sale: San Antonio Market Guide Manufactured Homes with Land Packages: How They Work

Manufactured Homes with Land Packages: How They Work

{kind=link}

{kind=link}

{kind=link}

{kind=link}