If you are researching an FHA loan for a modular home, the biggest thing to understand is this: FHA usually treats a modular home much more like a traditional site-built house, while FHA has extra, very specific rules for manufactured homes (often abbreviated as MH). Those differences affect what loan program you use, what the appraiser looks for, and what has to happen with the foundation, title, and land.

This guide breaks down the practical differences so you can choose the right path, especially if you are shopping for an affordable home around San Antonio.

Modular vs. manufactured (MH): the difference FHA cares about

These two home types can look similar in photos, but they are built under different standards.

- Modular homes are built in sections in a factory, then assembled on-site and generally must meet state and local building codes (often the IRC or local equivalents).

- Manufactured homes (MH) are built to the federal HUD Code (homes built after June 15, 1976). You will typically see HUD labels (tags) and a data plate inside.

Why this matters: FHA’s “default” home loan programs were designed for real property housing (like site-built). Modular usually fits that model smoothly. Manufactured can also qualify, but FHA adds requirements around permanent foundations, property classification, and, in many cases, land ownership.

For HUD’s overview of manufactured housing and the HUD Code, see HUD’s manufactured home information.

Which FHA loan is used for a modular home?

In most cases, an FHA loan for a modular home is simply a standard FHA-insured mortgage, similar to what a buyer would use for a site-built home.

That typically means a loan under FHA’s single-family programs (often referred to in the market as “standard FHA” purchase loans). Lenders still underwrite your income, debts, and credit, and the property still must meet FHA’s minimum property standards.

Key takeaway: Modular homes are commonly financed like site-built homes with FHA, as long as they are permanently affixed to a foundation and meet all local code and appraisal requirements.

For background on FHA-insured home loans, you can reference HUD’s FHA home loans page.

Which FHA loan is used for a manufactured home (MH)?

FHA financing for manufactured homes commonly falls into two buckets:

FHA Title II (mortgage on land + home)

FHA Title II is generally the best-known path when the manufactured home is treated as real property and financed similarly to a traditional mortgage.

In practice, Title II scenarios often require:

- The home is a HUD Code manufactured home.

- The home is on a permanent foundation that meets FHA/HUD requirements.

- The borrower typically owns the land (or is buying the land with the home), depending on lender requirements.

- The home is classified as real property (not personal property), which can require specific state steps.

FHA Title I (home only, or home in a community)

FHA Title I is designed to finance manufactured housing in ways that can be closer to “home-only” financing.

Title I is sometimes used when:

- You are financing the home without land, or

- The home will be placed in a manufactured home community (land lease), and the loan is structured as a personal property style loan.

Not every lender offers Title I, and terms/limits can differ from Title II. Homes2Go San Antonio summarizes these options on its financing page.

FHA loan for modular home vs. FHA for MH: the real-world differences

Here is the simplest way to think about it:

- Modular + FHA: usually follows “normal mortgage” logic.

- Manufactured (MH) + FHA: can follow mortgage logic (Title II) but adds extra property rules and documentation. Or it may use Title I, which can feel closer to “home-only” financing.

Quick comparison table

| Topic | FHA loan for modular home (typical) | FHA for manufactured home (MH) Title II (typical) | FHA for manufactured home (MH) Title I (typical) |

|---|---|---|---|

| Building standard | State/local building code | Federal HUD Code | Federal HUD Code |

| How it’s commonly underwritten | Like site-built | Like a mortgage (with MH-specific checks) | Often like home-only financing (program dependent) |

| Foundation expectations | Permanent foundation required for mortgage financing | Permanent foundation required (must meet FHA/HUD guidance) | May vary by lender/program, often not the same as Title II |

| Land | Usually included (real property) | Usually included (real property expectations) | May be home-only or land-lease situations |

| Titling/classification | Usually real property | Must meet state rules to be treated as real property | Often treated as personal property |

| Appraisal approach | Often uses site-built comps if appropriate | Uses manufactured home comps and HUD identifiers | May not follow a standard mortgage appraisal workflow |

This is a general comparison, not a lender quote. Exact requirements can vary by lender overlays and state/local rules.

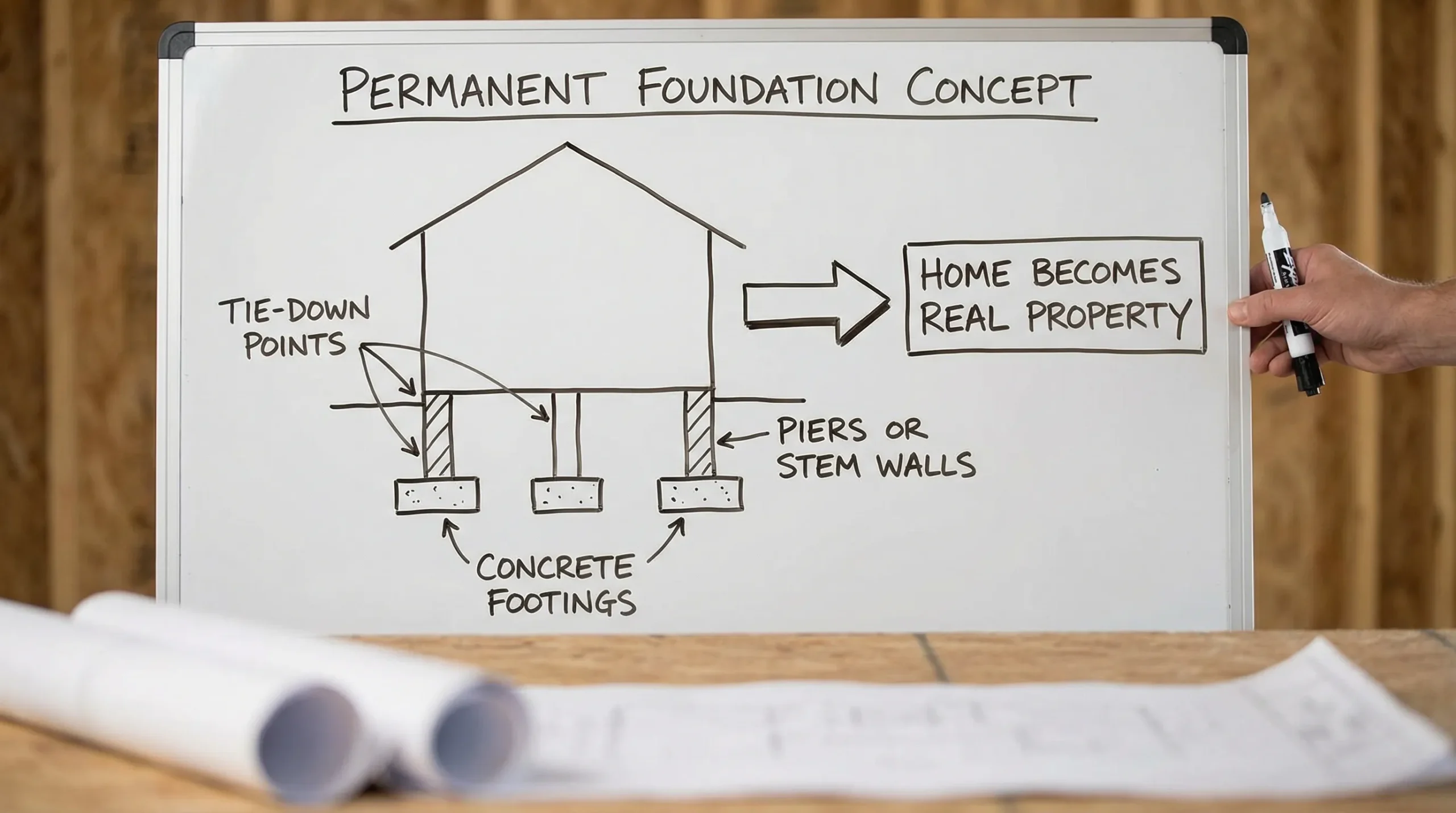

Property classification: “real property” is the pivot point

A major reason FHA for MH can feel more complicated than FHA for modular is the question: Is the home legally real property or personal property?

- Modular homes are usually set up to be real property once installed.

- Manufactured homes may start life with a title similar to a vehicle, then later be converted to real property depending on the state.

In Texas, classification and documentation steps can matter a lot for financing, taxes, and closing. If you are shopping around San Antonio and considering a land purchase, you may want to read Homes2Go’s guide to land and home packages in San Antonio, because combining land + home can simplify the “real property” path for many buyers.

Foundation and installation: why FHA scrutinizes MH more

FHA loans depend on the home being safe, sound, and secure, but manufactured homes get additional attention because of how they are built and transported.

Common MH Title II checkpoints include:

- Permanent foundation compliance (FHA references HUD foundation guidance for manufactured housing).

- Verification items like HUD labels/tags and the data plate.

- Installation consistency with state requirements and engineering, when applicable.

For modular homes, the lender still cares about the foundation and construction quality, but the workflow is closer to what lenders already do every day for site-built homes.

Appraisal differences: comps and documentation can change

Even when the same FHA lender offers both options, the appraisal process can differ.

Modular appraisals

A modular home appraisal often looks and feels like a site-built appraisal:

- Comparable sales may include site-built homes (if the market supports it).

- The appraiser focuses on typical real property items like condition, GLA, features, location, and market reaction.

Manufactured home appraisals (MH)

Manufactured home appraisals often require:

- Comparable sales that are also manufactured homes (when available).

- Verification of HUD identifiers.

- Closer attention to foundation and whether the home is treated as real property.

In some markets, finding strong manufactured home comps can be harder, which can affect timelines and outcomes. This is one reason many buyers start by talking to a retailer and lender early, before they fall in love with a specific home.

Down payment and mortgage insurance: similar headline numbers, different friction points

Consumers often hear about FHA because it is associated with lower down payments compared to some conventional scenarios. However, with manufactured homes, the “friction” is less about the down payment and more about meeting property requirements.

For modular homes financed with a standard FHA mortgage, the rules are usually more straightforward. For manufactured homes, even if the borrower is well-qualified, the deal can stall if the home cannot meet Title II property requirements.

For a consumer-friendly explanation of mortgage insurance and FHA basics, the CFPB’s mortgage resources are a helpful starting point.

What to ask lenders when comparing FHA modular vs. FHA MH

Before you apply, get clear answers to a few questions. This can save days (or weeks) later.

- Do you finance modular homes with a standard FHA mortgage? If yes, ask what documentation they require from the builder/installer.

- Do you offer FHA Title I or Title II for manufactured homes? Many lenders only do one.

- What foundation standard do you require for MH Title II? Ask how they document compliance.

- Do you require the land to be included? Some lenders require land ownership for certain manufactured home loan paths.

- How do you handle titling and conversion to real property in Texas? The closing process can depend on it.

Homes2Go San Antonio works with trusted local lenders and provides guidance through the process, which can be especially useful if this is your first purchase. You can start with their overview of manufactured home financing options.

San Antonio-specific practical advice (without the legal jargon)

Local factors can shape which path is easier.

- If you want to place a home on private land, your timeline may depend on utilities, access, septic (if needed), and local permitting. Homes2Go covers these steps in its land and home packages guide.

- If you are considering a community, confirm community rules early (age restrictions, home size, skirting requirements, exterior standards, etc.). Homes2Go’s mobile homes buyer guide for San Antonio explains community vs. private land tradeoffs.

None of these points are unique to FHA, but they influence whether a deal stays on-track.

So which is “better” for FHA: modular or manufactured?

If your goal is the smoothest FHA mortgage path, modular often behaves more like a normal home purchase, because:

- Building code alignment is more familiar to lenders and appraisers.

- Title issues are usually simpler.

- Appraisals can be more flexible in some neighborhoods.

That said, manufactured homes can still be an excellent value, especially for buyers who want move-in ready options and modern interiors at a lower price point. FHA can be a fit for MH too, but you should expect more property-specific requirements, particularly with Title II.

If you are not sure which home type fits your budget and timeline, it can help to compare floor plans and site requirements with a specialist before you lock in financing.

Frequently Asked Questions

Can you get an FHA loan for a modular home? Yes. In many cases, a modular home can be financed with a standard FHA-insured mortgage, similar to a site-built home, as long as it meets local code and lender property requirements.

How is an FHA loan for a modular home different from FHA for a manufactured home (MH)? Modular homes are typically treated more like site-built housing for underwriting and appraisal. Manufactured homes can qualify for FHA too, but often require specific HUD Code documentation, permanent foundation compliance, and the right property classification (especially for Title II).

Is FHA Title I or Title II better for manufactured homes? It depends on whether you are financing land with the home and whether the home can meet Title II property requirements. Title II is closer to a traditional mortgage. Title I can be used for certain home-only or community situations, depending on lender availability.

Do you need to own land to use FHA for a manufactured home? Often yes for Title II scenarios, but requirements vary by lender and program details. If you are in a land-lease community, Title I may be the more common FHA direction, if available.

What can delay FHA financing on a manufactured home? Common issues include foundation documentation, missing HUD tags/data plate information, challenges with comparable sales for appraisal, and unresolved titling or real-property conversion steps.

Talk to Homes2Go San Antonio about FHA-friendly options

If you are weighing an FHA loan for a modular home versus FHA financing for a manufactured home (MH), the fastest way to get clarity is to match the home type to your land plan, foundation needs, and lender requirements.

Homes2Go San Antonio can help you compare models, review floor plans, and connect with trusted local lenders who understand manufactured housing. Start here:

- Explore financing paths on the Homes2Go SA financing page

- If you are considering land, use the land and home packages guide

- For general shopping tips, read the San Antonio mobile homes buyer guide

When you are ready, reach out through the site to discuss your budget and which FHA route is most realistic for your timeline.

FHA Mortgage for Manufactured Home: Title and Foundation

FHA Mortgage for Manufactured Home: Title and Foundation Lot Rent for Mobile Home: What It Includes in Texas

Lot Rent for Mobile Home: What It Includes in Texas

{kind=link}

{kind=link}

{kind=link}

{kind=link}