A big reason people hesitate before buying a manufactured or “mobile” home is the question of value. Do mobile homes appreciate, or do they inevitably depreciate like a car?

The most accurate answer is: it depends on how the home is owned, titled, installed, and located, plus what’s happening in the local housing market. In San Antonio, where affordability matters and housing demand remains strong, manufactured homes can be a smart path to homeownership, but the value story looks different from a typical site-built home.

What “value” means for mobile and manufactured homes

When buyers search for the “value of mobile homes,” they are usually talking about one (or more) of these:

- Resale value: what a buyer will pay when you sell.

- Appraised value: what a licensed appraiser estimates based on comparable sales and property characteristics.

- Lending value: how a lender underwrites the collateral, which can differ based on whether the home is personal property or real property.

- Total wealth-building value: monthly cost savings versus renting, plus any appreciation of the home and land.

The key distinction is whether you are buying home-only (often in a land-lease community) or home plus land (land-owned, often financed as real estate).

Appreciation vs depreciation: what actually drives it?

A manufactured home can appreciate, hold value, or depreciate. The direction is mostly driven by the ownership structure and the “real estate fundamentals” around it.

1) Title and property classification (personal property vs real property)

This is one of the biggest drivers of long-term value behavior.

- Personal property (chattel): the home is titled more like a vehicle. This is common in land-lease communities.

- Real property: the home is legally tied to land (and usually installed to standards required for that classification). This is more common when you own the land.

In many markets, homes treated as real property tend to track real estate market dynamics more closely because buyers can use traditional mortgage products more often, and the land component can appreciate.

For Texas buyers, titling and ownership pathways often run through the state housing agency. The Texas Department of Housing and Community Affairs (TDHCA) is a key reference point for manufactured housing information and regulation.

2) Land: the silent driver of value

If you own the land, you are not only buying a home, you are buying a location and a scarce asset. In many areas, land appreciation is a major component of overall property appreciation.

If you lease the land (lot rent), your resale value depends more heavily on:

- The home’s condition and age

- Community desirability (rules, amenities, reputation)

- Lot rent levels and increases

- Whether the park allows buyer financing and smooth approval transfers

Homes in well-run communities can hold value better than people expect, but it is still a different value profile than owning land.

3) Age and standards (especially pre-1976 homes)

Manufactured homes built after the HUD Code took effect (June 15, 1976) are constructed to a federal building standard regulated by HUD. If you are comparing value over time, it helps to know what you are buying.

For background, see HUD’s overview of the manufactured housing program: HUD Manufactured Homes.

In many resale markets, older homes can face steeper headwinds (insurance, buyer financing, condition issues). Newer homes with modern layouts and energy features often compete more directly with entry-level site-built housing.

4) Installation quality, foundation, and permanence

Even a great home can lose value if it is poorly installed.

Buyers and appraisers tend to reward:

- Professional delivery and setup

- A foundation appropriate to the site and financing goals

- Good drainage and site prep (less moisture risk)

- Clear documentation of improvements and maintenance

If your long-term goal is appreciation-like behavior, the combination of land ownership plus a “real property” style setup is often the clearest path.

5) Financing availability (who can buy your home later?)

Resale value is not only about the home, it is about the future buyer’s ability to finance it.

- If most buyers must pay cash, demand can be thinner.

- If financing is widely available (and the home qualifies), you typically widen your buyer pool.

For a consumer-focused overview of manufactured housing finance and key terminology, the Consumer Financial Protection Bureau (CFPB) is a helpful starting point.

Homes2Go San Antonio explains common lending paths (including chattel and mortgage options) on its financing page.

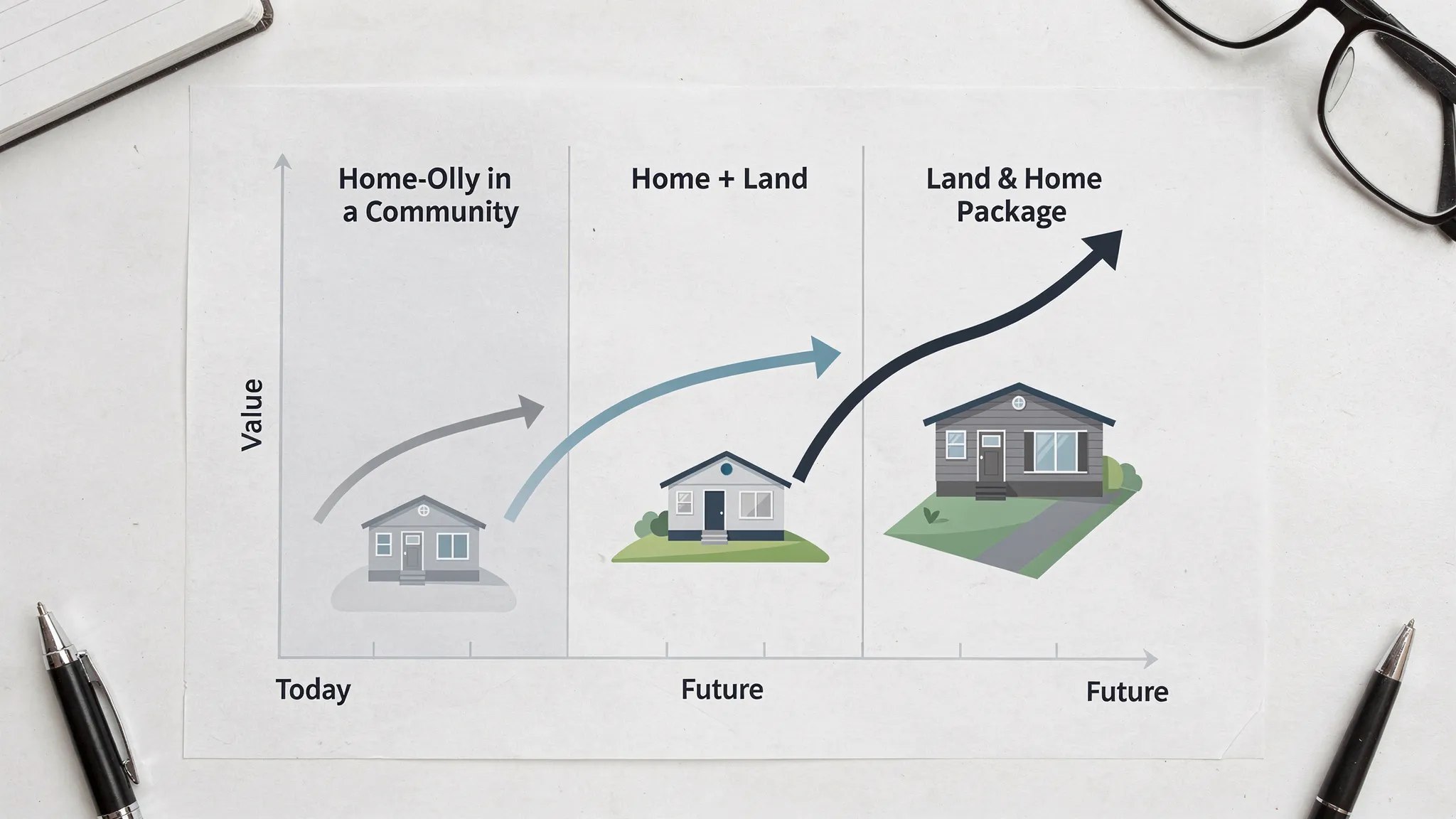

A practical way to think about mobile home value (common scenarios)

Instead of assuming “mobile homes depreciate,” it is more useful to match the purchase to the value pattern you are most likely to experience.

| Scenario | Typical ownership structure | What tends to happen to value over time | Why it behaves that way |

|---|---|---|---|

| Home in a land-lease community | Home-only, personal property is common | Often depreciates or stays flatter (varies by park and condition) | Value is driven mostly by the home itself, plus park desirability and lot rent trends |

| Home on owned land, titled as real property | Home plus land | More likely to behave like real estate (market-dependent) | Land can appreciate, buyer financing options may be broader |

| Land and home package | Home plus land (often planned from the start) | Often strongest long-term value profile among manufactured options | Installation, site prep, and financing are usually designed for real property outcomes |

| Older pre-1976 home | Varies | Can be harder to finance and insure, resale demand can be narrower | Standards, condition, and buyer constraints can reduce marketability |

If you are considering land ownership in the San Antonio area, Homes2Go’s guide on land and home packages can help you understand how that route works.

2026 trends shaping the value of mobile and manufactured homes

The value conversation is also influenced by broader housing forces. In 2026, a few themes matter most for buyers and sellers.

Affordability pressure keeps demand elevated

Across many U.S. metros, the affordability gap between entry-level site-built homes and manufactured housing remains meaningful. When monthly payments for conventional housing rise (because prices, rates, or both are high), demand for manufactured homes often strengthens, especially for buyers who want stability versus renting.

Interest rates change what buyers can afford

When rates rise, monthly payments rise too, which can cap how much buyers can pay. When rates fall, buyers often qualify for more. This is not unique to manufactured housing, but it affects resale liquidity and pricing.

If you are financing, it is smart to evaluate value through a monthly-payment lens, not only purchase price.

Energy efficiency is increasingly “value visible”

In Texas heat, buyers pay attention to insulation, windows, HVAC efficiency, and overall comfort. Efficient homes can become more desirable because they reduce operating costs.

Homes2Go San Antonio has a Texas-specific breakdown of what to look for in energy-efficient manufactured homes.

Community stability and lot rent sensitivity matter more

For land-lease buyers, the home’s value is tied to the community experience. Two trends can affect resale value:

- Lot rent increases can reduce what future buyers can afford monthly.

- Community rules and transfer approvals can impact how easily you can sell.

If you are shopping communities, this roundup of best mobile home parks in San Antonio (2025) is a useful starting point, even if you are comparing options in 2026.

What improves resale value (and what usually does not)

Manufactured home value is strongly influenced by the same buyer psychology that drives site-built value: condition, confidence, and monthly cost. Here are the upgrades and decisions that typically matter most.

The value drivers that tend to pay off

Condition and maintenance documentation: A clean, well-maintained home with records is easier to finance and easier to trust.

Durable “big ticket” items: Roof condition, HVAC performance, plumbing health, and moisture control are often more persuasive than cosmetic changes.

Curb appeal and site cleanliness: Simple landscaping, a tidy entry, and good skirting condition can change a buyer’s first impression.

Energy upgrades that reduce bills: Insulation improvements, efficient HVAC, and good windows can make the home more affordable month to month.

Location quality: In communities, that means park management, amenities, and rules. On land, that means access, drainage, flood risk, commute, and neighborhood trajectory.

What to be careful about (ROI can be unpredictable)

Some improvements are great for living quality but may not return dollar-for-dollar at resale:

- Highly personalized renovations

- Overbuilt outdoor structures that buyers may not value the same way

- Upgrades that are hard to document or verify

A helpful rule: prioritize safety, durability, and operating cost reductions first, then cosmetics.

How to estimate the value of a mobile home before you buy

If you want to avoid surprises later, evaluate the purchase the way an appraiser and a future buyer would.

Start with the “you can’t change it” factors

Focus first on:

- Location (community reputation or land location)

- Home specs (size, bed/bath count, layout)

- Age and HUD labels (confirm build info)

- Financing fit (does the home qualify for the type of loan you want?)

Homes2Go’s quick buyer guide walks through definitions, setup considerations, and common mistakes that can impact both financing and resale.

Then map the “all-in” cost that affects future demand

A buyer in 2028 or 2030 will still ask, “What will my monthly cost be?” So it is wise to evaluate costs that influence affordability.

| Cost category | Applies most to | Why it affects value | What to look for |

|---|---|---|---|

| Lot rent and fees | Land-lease community | Higher monthly cost can shrink buyer pool | Lot rent history, included utilities, fee schedule |

| Taxes and insurance | Land-home and some community setups | Total payment drives affordability | Quote insurance early, estimate taxes accurately |

| Utilities and efficiency | Both | Lower bills improve affordability | Insulation, windows, HVAC condition |

| Maintenance and replacements | Both | Deferred maintenance shows up as price pressure | Roof age, plumbing, moisture signs |

Use the right “comps” for your situation

Comps should match your ownership structure:

- If it is home-only, compare to other home-only sales in similar communities.

- If it is home plus land, compare to similar land-home properties, not just the home itself.

When in doubt, a licensed appraiser who regularly evaluates manufactured housing in your county can help you avoid comparing apples to oranges.

San Antonio-area factors that can move value up or down

Manufactured housing value is always local. In and around San Antonio, buyers should pay close attention to:

Flood risk and drainage: Even outside major floodways, poor drainage can cause long-term issues that hurt resale. Checking FEMA flood maps is a smart step. (Start with FEMA Flood Maps.)

Access to utilities and site costs (for land purchases): Septic, well, power runs, driveway access, and site prep can materially change the true cost basis of the property.

Permitting and compliance: Proper installation and documentation matters. If you are placing a home on land, confirm local requirements early.

Community rules (for land-lease): Pet policies, age restrictions, subletting rules, and buyer approval requirements all impact resale flexibility.

Where Homes2Go San Antonio fits in the value conversation

Value is not only what you pay, it is what you end up owning and how easily you can live in it, finance it, and eventually sell it.

Homes2Go San Antonio helps buyers navigate the big value levers by offering a wide selection of models, detailed floor plans, guidance through the buying process, and flexible financing options through trusted local lenders. If you are deciding between a community placement and a land-home route, you can also explore their resources on manufactured home options and costs and their financing overview.

The bottom line on the value of mobile homes

The “mobile homes always depreciate” idea is an oversimplification. A home-only purchase in a land-lease community often behaves differently than a manufactured home installed on owned land and treated as real property.

If your goal is long-term value, focus on the fundamentals that hold up over time: a desirable location, a home that qualifies for the financing you want, solid installation, good maintenance history, and monthly costs that stay competitive. In a market like San Antonio, those fundamentals can make manufactured homeownership both practical today and defensible when it is time to sell.

Manufactured Home Value: How to Estimate Accurately

Manufactured Home Value: How to Estimate Accurately Cost of Manufactured Homes: 2025 Price Breakdown

Cost of Manufactured Homes: 2025 Price Breakdown

{kind=link}

{kind=link}

{kind=link}

{kind=link}