Shopping mobile homes for sale and land can feel straightforward until you try to answer the only question that really matters: What will this cost me in total, not just at signing, but year after year?

The “home price” is only one line item. Land (or lot rent), site work, installation, financing structure, taxes, and insurance can change the true cost dramatically, even when two homes have similar floor plans.

This guide gives you a practical way to compare total costs across the most common buying paths in the San Antonio area, so you can make an apples-to-apples decision.

Start by identifying which “bundle” you are actually pricing

When buyers compare options, they often mix different deal types without realizing it. Each has a different cost profile.

Option A: Home in a land-lease community (you own the home, rent the lot)

You buy the manufactured home and pay monthly lot rent to the community.

Cost pattern: Lower upfront land cost, higher and rising monthly housing cost (lot rent), and community rules to follow.

Option B: Home + land you purchase separately

You buy land (or already own it) and buy a home, then pay for the site work and installation.

Cost pattern: Higher upfront work and coordination, more control long term, and you may build equity in land.

Option C: Land-home package (land and home planned together)

Land and home are coordinated as one plan (sometimes with a single closing), and site work may be scoped earlier.

Cost pattern: Often easier to budget because fewer “surprise” line items show up late, depending on what is included.

If you want the most “accurate” comparison, only compare options after you’ve translated each into the same cost categories below.

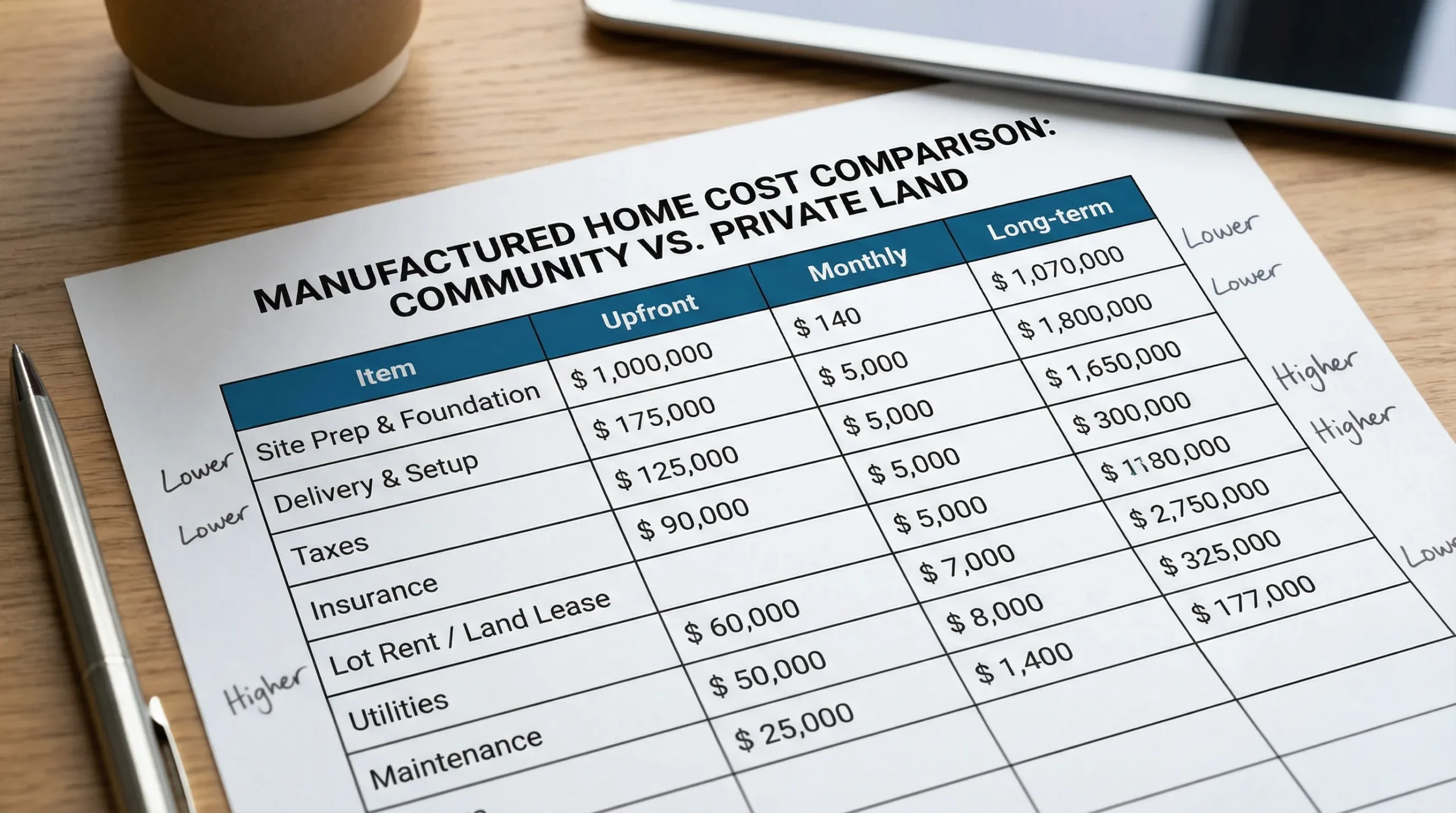

Use a simple 3-part framework: upfront, monthly, and long-term

A helpful way to compare is to separate costs into:

- Upfront costs (cash needed to close and move in)

- Monthly costs (what you must be able to afford every month)

- Long-term/ownership costs (repairs, replacements, resale costs, moving costs)

Here is a starting structure you can copy into a spreadsheet.

| Cost bucket | What it includes | Where it varies the most |

|---|---|---|

| Upfront | down payment, closing costs, land (if buying), site prep, delivery, installation, permits | raw land vs prepared lot, distance to utilities, foundation type, lender requirements |

| Monthly | loan payment, lot rent (if applicable), property taxes, insurance, utilities | chattel vs mortgage, tax classification, community rent increases |

| Long-term | maintenance, major replacements (roof/HVAC), septic service, resale and moving costs | home age, build quality, warranty, site conditions |

Upfront costs: what buyers commonly miss

For manufactured homes, the “move-in ready” promise depends on where the home is going and what infrastructure already exists.

1) Land or lot-related costs

If you are buying land, your upfront costs can include:

- Purchase price of the land

- Closing costs (title work, recording, lender fees)

- Survey (often required or strongly recommended)

- Clearing, grading, and driveway work

If you are renting a lot in a community, the equivalent “upfront” items can include:

- Community application fees

- Deposit(s)

- First month’s lot rent (and sometimes last month)

2) Site preparation (often the swing factor)

Site work is where budgets can change the fastest. A prepared lot with utilities at the pad is very different from raw land.

Common site-prep line items include:

- Home pad or foundation preparation (and related engineering, if required)

- Utility connections (water, electric, sewer or septic)

- Septic system (if not on municipal sewer)

- Well (if not on municipal water)

- Culvert/driveway access (especially in county areas)

- Drainage work and erosion control

Texas buyers should also understand that classification matters. Whether your home is treated as personal property or real property can affect financing, taxes, and closing structure. The Texas Department of Housing and Community Affairs (TDHCA) provides official guidance on manufactured housing, including the Statement of Ownership and Location (SOL): TDHCA Manufactured Housing.

3) Delivery, set, and installation

Even when a home price looks competitive, installation can add meaningful cost.

Typical items to confirm in writing:

- Delivery mileage and escort requirements

- Crane/set charges (if needed)

- Tie-downs/anchoring and leveling

- Steps, handrails, skirting

- Final trim-out and finish work (marriage line, touch-ups)

At the federal level, manufactured homes are built to the HUD Code, which sets construction and safety standards. That does not mean every site is equally easy to install on, but it helps explain why installation is its own scope: HUD Manufactured Home Construction and Safety Standards.

4) Permits, inspections, and local requirements

Permitting depends on whether you’re in the City of San Antonio, an incorporated area, or unincorporated Bexar County (or neighboring counties). Budget time and money for:

- Permit applications

- Inspections

- Address assignment (sometimes required before utilities)

A practical tip: ask your seller or retailer for a checklist based on your specific site address, not just “San Antonio.”

Financing: the same home can cost very different amounts depending on the loan

Your financing type can change both the monthly payment and the total interest paid over time. It can also change which closing costs appear upfront.

If you’re early in the process, Homes2Go San Antonio’s overview of pathways is a helpful reference: manufactured home financing options.

Here is a comparison framework (not rate quotes).

| Financing path | Common use case | What to watch when comparing total cost |

|---|---|---|

| Chattel loan (home-only) | home in a land-lease community, or home not permanently attached to real estate | shorter terms in many cases, different fee structures, insurance requirements, lot rent still applies |

| Land-home mortgage (real property) | home permanently sited on owned land (or land included) | appraisal and closing costs may be more like a traditional home loan, taxes/escrow often handled monthly |

| Government-backed programs (FHA/VA/USDA where eligible) | buyers seeking specific qualification benefits | property and installation requirements, appraisal conditions, timeline and documentation |

For a consumer-focused explanation of manufactured housing loan types and what questions to ask, the Consumer Financial Protection Bureau (CFPB) is a reliable source: CFPB guide to manufactured housing.

Two financing questions that prevent “payment shock”

Is lot rent included in the affordability calculation? Some buyers focus on the home payment and discover later that the combined monthly housing cost is too high.

Are taxes and insurance escrowed, or separate? If they are not escrowed, your monthly cash flow needs to cover them when due.

Monthly costs: build a realistic “all-in” housing number

Once the home is installed and you move in, your budget lives or dies on the monthly number.

If you rent a lot (community living)

Your monthly cost often includes:

- Home loan payment (if financed)

- Lot rent

- Utilities (some communities include certain services, many do not)

- Insurance

What to clarify before you commit:

- What lot rent includes (trash, water, sewer, amenities)

- How rent increases are handled and how often

- Community rules that could create extra costs (shed requirements, parking rules, pet rules)

Homes2Go’s community-focused roundup can help you think through what to compare on tours: mobile home parks in San Antonio.

If you own the land

Your monthly costs often include:

- Loan payment (may include land and home)

- Property taxes (land and home, depending on classification)

- Homeowners insurance (and possibly flood insurance)

- Utilities

- Septic service budgeting (if applicable)

A simple decision point is whether you prefer predictable monthly housing costs (often easier in a package where major site work is known earlier) or maximum long-term control (often stronger with owned land).

Long-term ownership costs: plan for the “year 5 to year 15” expenses

A total-cost comparison is incomplete if it ignores what happens after the new-home excitement fades.

Long-term costs to include in your worksheet:

- Routine maintenance (sealing, HVAC servicing, caulking, pest prevention)

- Major replacements (HVAC, water heater, roof at end of life)

- Re-leveling over time (site-dependent)

- Septic pumping and possible repairs (if on septic)

If there is any chance you will move the home again, understand that relocating a manufactured home can be expensive and sometimes impractical depending on age, condition, and route constraints. Even if you never move it, that reality can affect resale strategy.

How to compare two offers apples-to-apples (a practical method)

Instead of asking “Which option is cheaper?”, ask:

What is my total cost of ownership over my expected time horizon?

A clean way to do this is to compare 5-year and 10-year totals.

Step 1: Put every quote into the same worksheet

Create one sheet per option (community lot, owned land, land-home package). Use the same line items for each so blanks are obvious.

Recommended worksheet sections:

- Home price and included features

- Land price (if applicable)

- Site prep and utilities

- Delivery and installation

- Closing costs

- Monthly costs (loan, rent, taxes, insurance, utilities)

- Maintenance reserve (your own monthly set-aside)

Step 2: Use written numbers, not verbal estimates

For each option, aim to get:

- A written home quote with model and included items

- A written installation and delivery estimate

- A site work estimate (or a site inspection that narrows the range)

- A loan estimate or pre-approval that shows fees and cash-to-close

Verbal “ballparks” are useful early, but they are not a fair basis for comparing two options.

Step 3: Add a contingency line

Even well-planned installs can uncover surprises, especially on raw land.

A reasonable budgeting habit is to carry a contingency line for site work and utilities, then adjust it down only after you have site-specific quotes.

San Antonio-area cost drivers that deserve extra attention

Two buyers can choose the same home model and end up with different total costs because the land and local conditions differ.

Utility distance and availability

Extending power, water, or sewer can change the economics quickly. Before buying land, confirm:

- Where the nearest electric service point is

- Whether municipal water/sewer is available, and connection rules

- If not, what a well and septic plan would look like

Flood risk and drainage

Flood risk can influence site work, insurance, and long-term peace of mind. Check the address using official flood maps: FEMA Flood Map Service Center.

Soil and pad requirements

Soil conditions influence how much grading, base material, and drainage work you may need. If a site requires more engineering or more extensive pad preparation, your upfront costs can move.

City vs county jurisdiction

Permitting steps and timelines can differ depending on the exact location. Confirm requirements early so you do not get hit with delays that increase carrying costs.

When a land-home package can simplify total cost comparisons

Many buyers like the idea of land and home packages because they can reduce coordination risk.

Potential advantages, depending on what is included:

- Clearer scope early (land + installation plan)

- Fewer vendors to manage

- Financing that may align with real property when requirements are met

If you are considering this route, Homes2Go’s in-depth guide is a good companion to this cost framework: land and home packages in San Antonio.

A quick “total cost” checklist to bring to showings and calls

Use these questions to surface hidden costs fast.

Questions for the home quote

- What exactly is included in the base price (appliances, skirting, steps, setup items)?

- What is excluded that buyers commonly assume is included?

- What warranties apply, and who handles service?

Questions for land (or a land-home plan)

- Are utilities at the pad, or do they need to be extended?

- Is septic required, and has a feasibility check been done?

- Are there access issues for delivery (roads, turns, gates, overhead lines)?

Questions for communities (if renting a lot)

- What does lot rent include, and what is billed separately?

- How are rent increases handled?

- Are there requirements that create extra costs (fencing, sheds, carports, landscaping)?

Putting it all together: the decision is usually about risk, not just price

If you only compare the sticker price of the home, you can end up choosing the option with the lowest visible number but the highest total cost.

A more reliable approach is:

- Choose your likely living situation (community lot vs owned land)

- Demand written scope for installation and site work

- Compare monthly costs with taxes, insurance, and lot rent included

- Evaluate long-term control and resale strategy

If you want help turning quotes into a clear monthly and total-cost picture, Homes2Go San Antonio can walk you through models, floor plans, and financing pathways, then help you line up the right next steps for your site or community plan. Start by browsing their buyer resources or reaching out for guidance: Mobile homes buyer guide.

Land and Manufactured Home Packages: Timeline, Costs, Financing

Land and Manufactured Home Packages: Timeline, Costs, Financing Double Wides for Rent Near Me: What You’ll Pay and What to Ask

Double Wides for Rent Near Me: What You’ll Pay and What to Ask

{kind=link}

{kind=link}

{kind=link}

{kind=link}