When you buy land and a manufactured home separately, you can end up juggling two closings, two sets of deadlines, and a long list of contractors. Land and manufactured home packages simplify that process by bundling key steps, but the experience still depends on one thing: planning for the real timeline, the real cost drivers, and the financing path that fits your land and your home.

This guide breaks down what to expect, where delays usually happen, how budgets typically get built, and which financing options are most common for buyers around San Antonio.

What a land and manufactured home package usually includes (and what it doesn’t)

A “package” can mean different things depending on who is offering it and whether you’re buying in a developed community or on private land. In general, a land and home package is designed to coordinate the two biggest pieces of the purchase:

- The homesite (land purchase, or a lot in a community)

- The manufactured home (either an inventory home or a custom order)

What may or may not be included in a package is the important part.

Often included

- Help selecting a home model and reviewing floor plans

- Coordination between the home order, delivery, and installation schedule

- Guidance on financing options (land-home mortgage vs chattel, and lender requirements)

- Basic direction on what site work is needed for your land

Sometimes included (confirm in writing)

- Utility connections (water, sewer or septic, electric)

- Driveway, culvert, and grading

- Permits and inspections coordination

- Foundation type (pier and beam vs slab) and tie-downs

- Appliances, decks, steps, skirting, and storage

Because packages vary so much, the smartest move is to request a written scope that separates:

- Home costs

- Land costs

- Site work and installation costs

- Fees and closing costs

If you want a deeper primer on how packages work in the San Antonio area, Homes2Go also has a more comprehensive overview here: land and home packages in San Antonio.

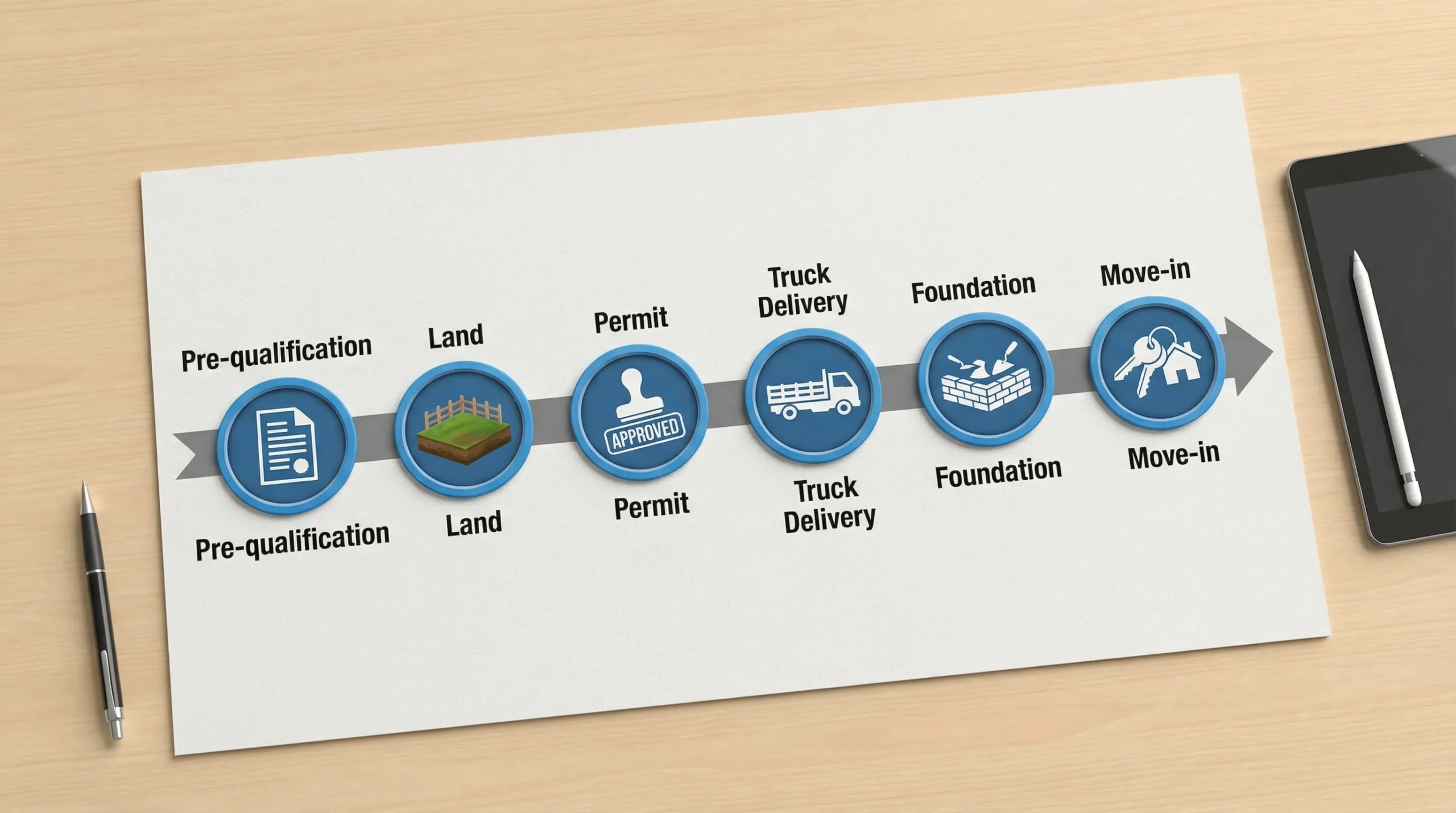

Timeline: what the process looks like from pre-approval to move-in

A realistic timeline helps you avoid two common problems:

- Running out of rate-lock time (or needing an extension)

- Paying for site work too early (before permits, utility confirmations, or lender approval)

Here is a practical, buyer-focused timeline you can use to plan.

Typical phases and time ranges

| Phase | What happens | Common time range (varies by land and lender) |

|---|---|---|

| 1. Pre-qualification and budget | Credit, income review, rough budget, lender fit (land-home vs chattel) | A few days to 2 weeks |

| 2. Choose land and home | Select lot/land, pick home model (inventory vs order), start documentation | 1 to 4 weeks |

| 3. Site evaluation and planning | Soil and slope review, utilities confirmation, septic planning if needed, access for delivery | 2 to 8+ weeks |

| 4. Permits and underwriting | Permitting, appraisal (if applicable), underwriting conditions, insurance quotes | 3 to 8+ weeks |

| 5. Home delivery and installation | Delivery scheduling, foundation/tie-downs, utility hookups, steps/skirting (if included) | 2 to 6 weeks |

| 6. Inspections and closeout | Final inspections, corrections, titling or real-property steps, final lender sign-off | 1 to 4 weeks |

These phases can overlap, but the critical path usually runs through utilities, permitting, and lender requirements.

The biggest timeline swing factors (what moves your move-in date)

-

Inventory home vs custom order: Inventory and move-in ready homes can shorten the schedule dramatically. Custom builds add production lead time.

-

Utilities and septic: On raw land, confirming water source, septic feasibility, and electric availability can take longer than buyers expect.

-

Permitting differences by location: City, county, and subdivision rules can change what you need to submit and how long approvals take.

-

Loan type: A land-home mortgage typically has more steps than a chattel loan, especially around appraisal and permanent foundation requirements.

Costs: a clear way to budget without surprises

Instead of trying to guess one “all-in” number, it’s more useful to understand the cost buckets and when they tend to hit. Your total cost is typically made up of:

- Home (the unit itself, options, upgrades)

- Land (purchase price, survey, title work)

- Site work and installation (prep, foundation, utilities, delivery, setup)

- Financing and closing (origination, third-party fees, escrow, taxes, insurance)

A cost breakdown you can use in conversations with lenders and retailers

| Cost bucket | What it can include | When it usually happens |

|---|---|---|

| Home and options | Base home price, interior options, energy upgrades, appliances (if selected) | At order, at closing, or split depending on contract |

| Delivery and set | Transportation, crane (if needed), blocking, tie-downs, leveling | Around delivery and installation |

| Foundation | Pier and beam or slab (depends on loan and site) | Before installation or during set |

| Site prep | Clearing, grading, driveway, culvert, pad | Before delivery |

| Utilities | Electric pole or connection, trenching, water line, septic system, hookups | Before and after delivery (varies by trade) |

| Permits and inspections | Local permits, third-party inspections where required | Early to mid-project |

| Land transaction costs | Survey, title work, recording, sometimes HOA documents | Before land closing |

| Loan and closing costs | Lender fees, appraisal (if required), escrow setup, prepaid taxes/insurance | At closing |

Two cost categories buyers often underestimate

1) “Access” costs

Manufactured home delivery requires a path for a large transport and setup crew. Tight turns, soft soil, low branches, and narrow gates can add unplanned work.

2) “Utility distance” costs

Even when utilities exist “at the road,” the cost can change based on how far your home pad is from the connection point, and whether trenching crosses rock, caliche, or drainage areas.

Financing: which options fit land and manufactured home packages

Your financing choice affects your timeline, your documentation, and sometimes the installation requirements.

Homes2Go San Antonio outlines common options on its manufactured home financing page. Below is a decision-friendly view of how these options usually map to package purchases.

Financing options at a glance

| Financing path | Often a good fit when… | Key considerations |

|---|---|---|

| Land-home mortgage (single loan) | You want land + home together, and the home will be real property | Typically requires a permanent foundation and an appraisal. Documentation can be heavier, but it can simplify long-term ownership. |

| Chattel loan (home only) + land separately | You already own land, or you’re buying land with cash or a separate loan | Can close faster for the home, but you still need to coordinate site work and land ownership steps carefully. |

| Construction-to-permanent style setup | Your project involves multiple site-work steps and lender-managed draw timing | Not available in every scenario, and requirements vary by lender. Useful when the lender wants a structured build process. |

| Community purchase or land-lease | You prefer a community setting with managed infrastructure | Land-lease means you pay lot rent. Buying a lot in a community is different than leasing, confirm which applies. |

How to choose the “right” financing path

The fastest way to narrow it down is to answer three questions:

Will you own the land at closing? If yes, you may qualify for land-home financing depending on lender rules.

Will the home be classified as real property? Many mortgage-style options require the home to be affixed to land you own and meet specific foundation and titling criteria.

Is your land build-ready? If utilities and permits are complicated, a lender may require more documentation or a different structure.

For a baseline definition of what qualifies as a manufactured home under the HUD Code (and how it differs from other housing types), you can review HUD’s manufactured housing program overview at HUD.gov.

Underwriting checkpoints: what lenders look for on land + manufactured home deals

Even strong buyers get delayed by missing items that are specific to manufactured homes and land.

Property and home requirements that commonly trigger conditions

- HUD labels and data plate: Lenders and insurers often require verification that the home is a HUD Code manufactured home.

- Foundation and installation compliance: Depending on the loan type, the lender may require a specific foundation standard and documentation from licensed installers.

- Utilities and habitability: The home typically must have legal access, water, and power to meet occupancy requirements.

- Appraisal complexity: Land plus manufactured home appraisals can take longer, particularly when comparable sales are limited in a micro-area.

Borrower documentation that speeds things up

- Recent paystubs or proof of income

- W-2s or tax returns (especially for self-employed borrowers)

- Bank statements showing down payment and reserves

- Land contract or proof of land ownership

- Any known HOA or subdivision documentation (if applicable)

If you are self-employed or run a small company, underwriting often hinges on clean, consistent financial reporting. In those cases, improving how your business tracks revenue, expenses, and statements can genuinely reduce friction. Some owners modernize their back office with tools and consulting support such as AI & NetSuite consulting so financials are easier to produce and explain when large purchases come up.

Common delay points (and how to prevent them)

Delays are rarely caused by one big problem. They usually come from small gaps that compound.

Permit and jurisdiction surprises

Before you commit to land, confirm:

- Which authority issues permits (city vs county)

- Whether the road is public or private

- Whether a septic permit is needed, and what the lead time is

A quick call to the permitting office, or a conversation with a local home consultant who has done installs in that area, can save weeks.

Site work started too early

It’s tempting to start clearing and grading as soon as you “know” you want the property. But if a lender appraisal, survey, or permit requires changes to pad location, drainage, or setbacks, you can end up paying twice.

A safer approach is to complete a basic site plan first, then schedule work in this order:

- Confirm access and home placement

- Confirm utility plan (water, power, septic or sewer)

- Pull permits where required

- Schedule site prep

Insurance timing

Insurance can become a last-minute scramble, especially if the home location is rural or if there are fewer carriers available for certain setups.

Get quotes early, and confirm with your lender what coverage and effective dates are required for closing.

A practical “buyer plan” for the next 30 to 60 days

If your goal is to purchase within the next couple of months, focus less on perfecting the home’s finish selections and more on eliminating the biggest sources of uncertainty.

Priorities that keep packages on track

- Get pre-qualified first so you shop with a realistic payment range.

- Choose the financing path early (land-home vs chattel) because it affects foundation, timeline, and paperwork.

- Treat utilities like a first-class decision, not an afterthought. Water and septic answers can determine whether a “great deal” is actually viable.

- Ask for an itemized estimate that separates home, land, site work, and fees so you can compare apples to apples.

How Homes2Go San Antonio can help

Homes2Go San Antonio focuses on helping buyers pair an affordable manufactured home with a workable path to ownership in the San Antonio area, including model selection, guidance through the process, and flexible financing options through trusted local lenders.

If you want to explore next steps, you can:

- Review financing pathways on the financing page

- Browse the community land option highlighted on the property page

- Compare home types and price drivers in the manufactured homes buyer guide

The main takeaway is simple: land and manufactured home packages can be a smoother way to buy, but only when the timeline, site work scope, and financing structure are aligned from day one.

Affordable Mobile Homes for Rent: Real Monthly Cost Breakdown

Affordable Mobile Homes for Rent: Real Monthly Cost Breakdown Mobile Homes for Sale and Land: How to Compare Total Costs

Mobile Homes for Sale and Land: How to Compare Total Costs

{kind=link}

{kind=link}

{kind=link}

{kind=link}