Buying a “mobile home” with an FHA loan is possible, but FHA has very specific rules about the borrower, the home, and the way it’s installed and titled. If you’re shopping for an affordable manufactured home in the San Antonio area, understanding those rules upfront can save you weeks of back-and-forth with lenders and prevent last-minute surprises during appraisal or underwriting.

This guide breaks down FHA loans for mobile homes, what typically qualifies, and the practical steps to go from “I’m interested” to “clear to close.”

First, what FHA means by “mobile home”

In most financing conversations, FHA is talking about a manufactured home built to the federal HUD Code (generally homes built on or after June 15, 1976). Older “mobile homes” can be harder or impossible to finance with FHA, depending on age, condition, and documentation.

If you’re unsure what you’re looking at, ask for the home’s HUD compliance information (often called the HUD data plate) and confirm the build date.

FHA eligibility for manufactured homes (the big requirements)

FHA eligibility is a three-part puzzle:

- You, as the borrower

- The manufactured home itself

- The land, foundation, and legal/titling setup

Borrower basics FHA lenders look for

FHA loans are known for being more flexible than many conventional mortgages, but you still need to show you can repay the loan.

Most FHA lenders will evaluate:

- Occupancy: The home must be your primary residence.

- Income and employment: Stable, documentable income (W-2, 1099, or other verifiable sources).

- Credit profile: FHA guidelines allow lower down payments with stronger credit, but individual lenders may add “overlays” (stricter rules).

- Debt-to-income (DTI): Your monthly debts compared to your monthly income.

If you’re early in the process, the fastest way to get clarity is a lender pre-approval (not just a pre-qualification).

Home requirements (what FHA will typically require)

For FHA-insured financing, manufactured homes generally must meet requirements tied to safety, permanence, and marketability, including:

- HUD Code construction (manufactured home, not an RV or travel trailer)

- Permanent foundation that meets FHA requirements and local codes

- Utilities and year-round access (water, sewer/septic, power, and legal access)

- Appraisal standards: The home has to appraise, and the appraiser must be able to support the value with comparable sales

For official program details, you can review HUD’s overview of the FHA manufactured home lending programs, including the FHA Title I manufactured home loan program.

Titling matters more than most buyers expect

One of the biggest “gotchas” with manufactured housing is whether the home is treated as personal property (similar to a vehicle title) or real property (like a typical house).

In many cases:

- FHA mortgage-style financing is easier when the home is permanently affixed and titled/recorded as real estate.

- If a home is still titled as personal property, the lender may require steps to convert or “retire” that title depending on the loan structure and Texas requirements.

Because titling steps can be procedural and time-sensitive, it’s smart to raise this question before you spend money on appraisal or engineering.

FHA Title I vs Title II for manufactured homes

There are two common FHA pathways people mean when they say “FHA loan for a mobile home.” The right one depends on whether you’re financing just the home, or the home plus land as real estate.

| FHA option | Common use case | Typical collateral | Best fit when… |

|---|---|---|---|

| FHA Title I | Financing a manufactured home (sometimes with a lot) | Often treated more like personal property financing | You’re buying a home without a traditional mortgage setup, or you need flexibility around land ownership (program and lender rules vary) |

| FHA Title II | FHA mortgage for manufactured home + land | Real property (home and land together) | You’re placing the home on owned land (or buying land with it) and can meet mortgage, foundation, and titling requirements |

The practical takeaway: if your plan is a land + home package with a permanent foundation, many buyers pursue an FHA mortgage structure. If you’re buying only the home in a land-lease community, the financing path may look different.

If you’re comparing ownership setups, this Homes2Go SA guide on land and home packages in San Antonio is a helpful companion read.

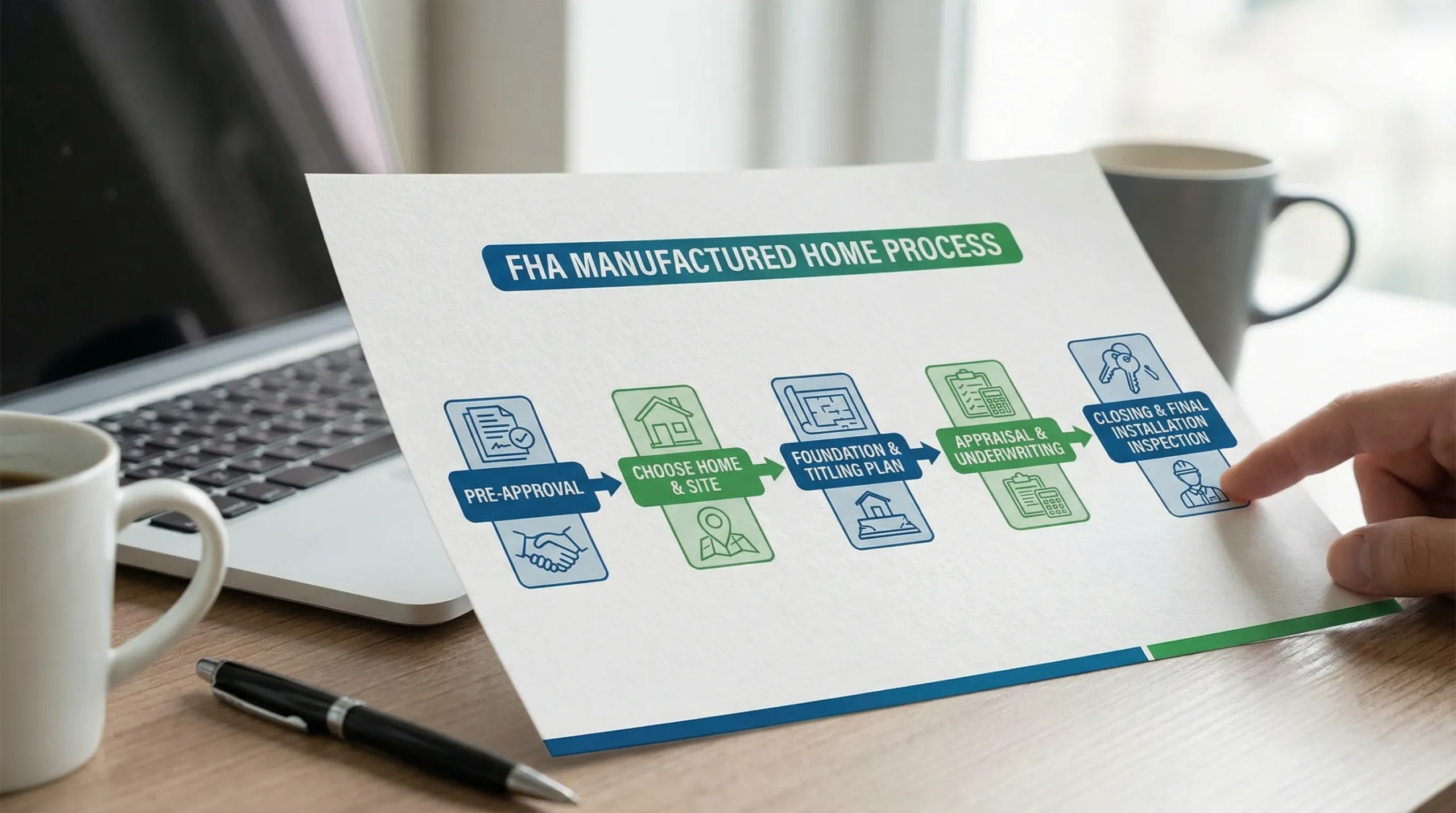

Steps to finance a manufactured home with FHA (from start to keys)

Below is the process most buyers experience, with notes on where manufactured homes differ from site-built homes.

Step 1: Pre-approve with a lender who does manufactured homes

Not every lender that “does FHA” is comfortable with manufactured housing. Start by asking directly:

- Do you offer FHA financing for manufactured homes?

- Do you finance homes in land-lease communities, private land, or both?

- What foundation and titling documentation do you require?

A lender experienced in manufactured homes can flag potential issues early, like property type, appraisal concerns, or title status.

Step 2: Choose the right home type for your financing plan

Before you fall in love with a floor plan, align the home with your FHA route:

- HUD Code manufactured home vs modular vs older mobile home

- New home vs used home (used can be financeable, but condition, documentation, and comps matter)

- Single section vs multi section (financing and appraisal can differ by lender appetite)

Homes2Go San Antonio can walk you through available models and floor plans so you can match your budget to a home that fits lender requirements without guesswork.

Step 3: Confirm the site plan, foundation plan, and utilities

For FHA mortgage-style financing, the site and installation plan are not “later” details. They are central to underwriting.

You typically need clarity on:

- Where the home will be placed (address and legal description)

- How it will be installed (foundation type, tie-downs, and code compliance)

- Utility connections (water, sewer/septic, electric)

- Permits and inspections required locally

In the San Antonio area, these details can vary based on whether you’re placing the home in a community, on private land, or in an area with specific zoning or floodplain considerations.

Step 4: Get a written estimate of all-in costs

Manufactured home affordability is real, but buyers get surprised when they focus only on the home price.

Ask for a clear estimate that separates:

- Home price

- Delivery and setup

- Site work (pad, driveway, grading)

- Utility runs

- Permits, inspections, and any required engineering

This total matters because lenders qualify you based on the full monthly housing expense, not just the base home.

Step 5: Apply, disclose documents, and lock your loan details

Once you’re under contract (or have an agreed purchase plan), you’ll submit your full application and documentation.

At this point, your lender will also confirm which FHA track is being used and what property documentation is required (especially around foundation and titling).

Step 6: FHA appraisal and underwriting

The appraisal stage is where manufactured homes can become tricky.

Common appraisal challenges include:

- Limited comparable manufactured home sales in the immediate area

- Condition issues or required repairs (handrails, broken windows, roof issues, missing smoke detectors, etc.)

- Questions about whether the home is permanently affixed and marketable as real estate

Underwriting then ties everything together: income, credit, DTI, asset sourcing, and property acceptability.

Step 7: Closing, installation, and final sign-offs

For a manufactured home, “closing” is not always the final milestone. Depending on your structure, the lender may require proof of proper installation and final inspections.

Your timeline can also depend on:

- Permit processing

- Utility scheduling

- Weather and site readiness

Setting expectations early helps you plan move-out dates, storage, and lease end dates realistically.

Common FHA obstacles for manufactured homes (and how to avoid them)

A few issues account for most financing delays.

Missing HUD labels or data plate info

If the HUD tags/data plate details are missing, the lender and appraiser may not be able to verify the home’s compliance. For used homes, confirm documentation early.

Foundation documentation doesn’t match lender requirements

Even when a home is installed correctly, lenders often need specific documentation (for example, an engineer’s letter or certification depending on the situation). Ask what’s needed before install so you don’t pay twice.

Title and recording are unclear

If the home is still treated as personal property, you may need extra steps (and time) to align it with the loan type. Clarify whether the transaction is expected to close as real estate.

Appraisal comes in low

Low appraisal risk is real in any market, but it can be higher when comparable manufactured home sales are limited. Ways to reduce the risk include choosing a location with established manufactured home values and keeping upgrades/documentation organized.

A lender-ready checklist (what to gather before you apply)

Having these items ready speeds up underwriting and reduces the number of “conditions” you’ll be asked to clear.

- Government-issued photo ID

- Recent pay stubs and two years of W-2s (or tax returns if self-employed)

- Recent bank statements (for down payment and reserves)

- Permission for the lender to pull credit

- Home details (make/model, year built, serial/VIN, HUD labels if available)

- Site details (address, land ownership, and an outline of utilities and installation plan)

If lender conversations make you nervous, it can help to practice your questions out loud. Some teams and professionals use AI roleplay tools to build confidence and handle objections in high-stakes conversations, for example Scenario IQ’s AI roleplay training. As a buyer, you can borrow the same idea by rehearsing how you’ll explain your income, debts, and down payment plan before you ever submit an application.

How Homes2Go San Antonio fits into the FHA process

Homes2Go San Antonio focuses on helping buyers find affordable manufactured housing options and navigate the purchase with experienced guidance. If you’re exploring FHA financing, the most helpful ways a retailer can support you are practical:

- Narrowing home choices to models that align with your financing and installation plan

- Providing detailed floor plans and specifications when your lender requests them

- Coordinating timing between your lender, installer, and any community or land requirements

- Connecting you with trusted local lenders (so you can compare options and overlays)

If you’re still deciding between home types and financing paths, this mobile homes San Antonio buyer guide can help you map out the decision.

Bottom line

FHA loans can be a strong tool for manufactured home buyers, but the home must meet HUD and FHA requirements, and the foundation, land, and titling details have to match the loan structure. Start with a lender who regularly finances manufactured homes, confirm the HUD Code and documentation, and treat site planning as part of financing, not an afterthought.

When those pieces are aligned early, the FHA process becomes much more predictable, and you can focus on what matters: choosing a home that fits your budget and your life in San Antonio.

Manufactured Homes with Land Packages: How They Work

Manufactured Homes with Land Packages: How They Work Manufactured Homes for Sale San Antonio: What to Know

Manufactured Homes for Sale San Antonio: What to Know

{kind=link}

{kind=link}

{kind=link}

{kind=link}