FHA loans can make buying a manufactured (mobile) home far more achievable, especially for first-time buyers, but “FHA financing for mobile homes” does not mean every home qualifies or that FHA covers the same things in every situation. What’s covered depends on which FHA program you use, how the home is titled, and whether it’s treated like real estate.

Below is a clear, buyer-friendly breakdown of what FHA financing can cover for mobile homes, what it typically does not cover, and what to prepare for if you’re shopping in the San Antonio area.

First, what FHA means by “mobile home”

In everyday conversation, people say “mobile home” for anything factory-built. For FHA eligibility, the key distinction is usually manufactured home vs older mobile home.

- Manufactured home (HUD Code): Built on or after June 15, 1976 and constructed to the federal HUD Code. These homes should have a HUD data plate and HUD certification labels.

- Pre-1976 mobile home: Often does not meet FHA eligibility.

If you’re unsure, your retailer and lender can help you verify the build date and HUD labeling before you spend money on inspections, appraisals, or engineering.

The two FHA options that matter: Title I vs Title II

When people search for “FHA financing for mobile homes,” they’re typically referring to one of these two pathways:

| FHA path | Best for | What’s being financed | Common real-world scenario |

|---|---|---|---|

| FHA Title I (Manufactured Home Loan) | Buyers who are not doing a traditional mortgage, often in land-lease communities | Home only, lot only, or home + lot (program rules apply) | Buying a manufactured home in a community where you lease the homesite |

| FHA Title II (Traditional FHA mortgage) | Buyers purchasing land and permanently affixing the home | Home + land as real property with a standard FHA mortgage | Buying a land-and-home package, or placing the home on your own land |

You can read the program overviews directly from HUD: FHA Title I and FHA-insured single-family mortgages (Title II).

What FHA financing for mobile homes can cover

Coverage depends on whether you’re using Title I or Title II, but in general, FHA-backed financing can help cover the home, the site, and certain costs required to make the home livable and financeable.

1) The manufactured home purchase (the unit itself)

Both FHA Title I and Title II are designed to finance the purchase of an eligible manufactured home.

To be eligible, the home typically must:

- Be a HUD Code manufactured home (generally built on/after June 15, 1976)

- Be one-family and meet minimum size and safety standards

- Be your primary residence (FHA is not meant for second homes or pure investments)

2) The land (sometimes)

This is where “what’s covered” starts to diverge.

- FHA Title II usually finances home + land together, similar to a traditional house purchase, assuming the home is treated as real property.

- FHA Title I can, in some cases, finance the lot or home + lot, and it is often discussed for scenarios where the buyer is not using a standard mortgage.

If you’re deciding between community living vs private land, it helps to read a broader local overview first, then return to financing details. Homes2Go’s buyer guide is a good starting point: Mobile Homes San Antonio: A Quick Buyer Guide.

3) Costs required to install and make the home “mortgage-ready” (common with Title II)

When you finance a manufactured home as real estate (Title II), the lender and appraiser typically need to see that the property meets FHA’s standards for safety, security, and structural soundness. In practice, that often means FHA financing may be used to cover costs tied to a compliant setup, such as:

- Permanent foundation work that meets FHA criteria

- Tie-downs/anchoring and installation requirements

- Utility connections (water, sewer/septic, electric) needed for livability

- Site-related work required for access and basic function (for example, meeting local requirements for ingress/egress)

Whether these costs are wrapped into the loan depends on loan structure, appraisal, and lender guidelines. In San Antonio, many buyers explore this through a coordinated approach like a land-and-home package. If that’s your goal, see: Land and Home Packages San Antonio: Complete Guide.

4) Standard homebuying closing costs (with lender rules)

FHA loans can include typical closing-related expenses (exact treatment varies by lender and transaction), including items like:

- Appraisal and credit report fees

- Title work (when applicable)

- Prepaid items and escrow setup (taxes, homeowners insurance)

Also, FHA transactions often allow seller concessions (within FHA limits and based on what your lender approves), which can reduce your out-of-pocket cash at closing.

5) Mortgage insurance (it’s part of FHA coverage, but it’s a cost)

FHA loans typically require mortgage insurance, which is one reason FHA is able to approve borrowers with smaller down payments. This is not a “benefit” in the sense of free coverage, but it is part of how the program works.

For a plain-English overview of FHA mortgage insurance concepts, you can reference the Consumer Financial Protection Bureau’s mortgage resources.

What FHA typically does not cover for mobile homes

Many disappointments happen when buyers assume FHA will finance any “mobile home.” Here are common deal-breakers.

| Not typically covered | Why it matters |

|---|---|

| Pre-1976 mobile homes | Often not HUD Code compliant, so they fail basic FHA eligibility standards |

| Homes without HUD labels/data plate | Lenders/appraisers may not be able to validate eligibility |

| Second homes and most investment-only purchases | FHA is primarily for owner-occupied primary residences |

| Properties that cannot meet FHA appraisal requirements | Safety, structural, access, and utility issues can stop approval |

| A setup that cannot qualify as real property (for Title II) | If the home is not on an acceptable permanent foundation (and properly titled), a traditional FHA mortgage may not be possible |

If you’re considering an older home because it looks like a bargain, build the financing reality into your decision early. Sometimes a home that “costs less” becomes more expensive when you factor in the loan you can (or cannot) get.

The big eligibility factors FHA lenders look for

FHA rules and lender overlays can get technical, but most approvals hinge on a few practical checkpoints.

Home requirements (the unit)

Expect the lender and appraiser to verify:

- HUD Code compliance (build date, HUD labels, data plate)

- Condition that can pass FHA’s appraisal standards

- That it’s a single-family residence

Foundation and title (especially for Title II)

For an FHA mortgage (Title II), manufactured homes generally must be treated like real estate, which usually means:

- The home is permanently affixed to an acceptable foundation

- The home is titled and recorded in a way the lender can place a mortgage lien (how this works can be state-specific)

In Texas, manufactured home ownership and location documentation often runs through the Texas Department of Housing and Community Affairs (TDHCA). Start here for official info: TDHCA Manufactured Housing.

Land or community requirements

Whether you’re buying land or leasing a lot in a community, the lender will care about basics like:

- Legal access (ingress/egress)

- Utilities and wastewater method (public sewer vs septic)

- Flood hazards and insurance requirements, where applicable

- Zoning and local placement rules

Borrower requirements (credit, income, occupancy)

FHA underwriting is borrower-focused, too. Common themes include:

- Primary residence occupancy

- Verifiable income and employment history (documentation varies)

- A credit profile that meets FHA and lender requirements

Down payment requirements vary by credit and lender policy. Many buyers hear “3.5% down” because FHA allows that in certain credit scenarios, but your lender will confirm what applies to you.

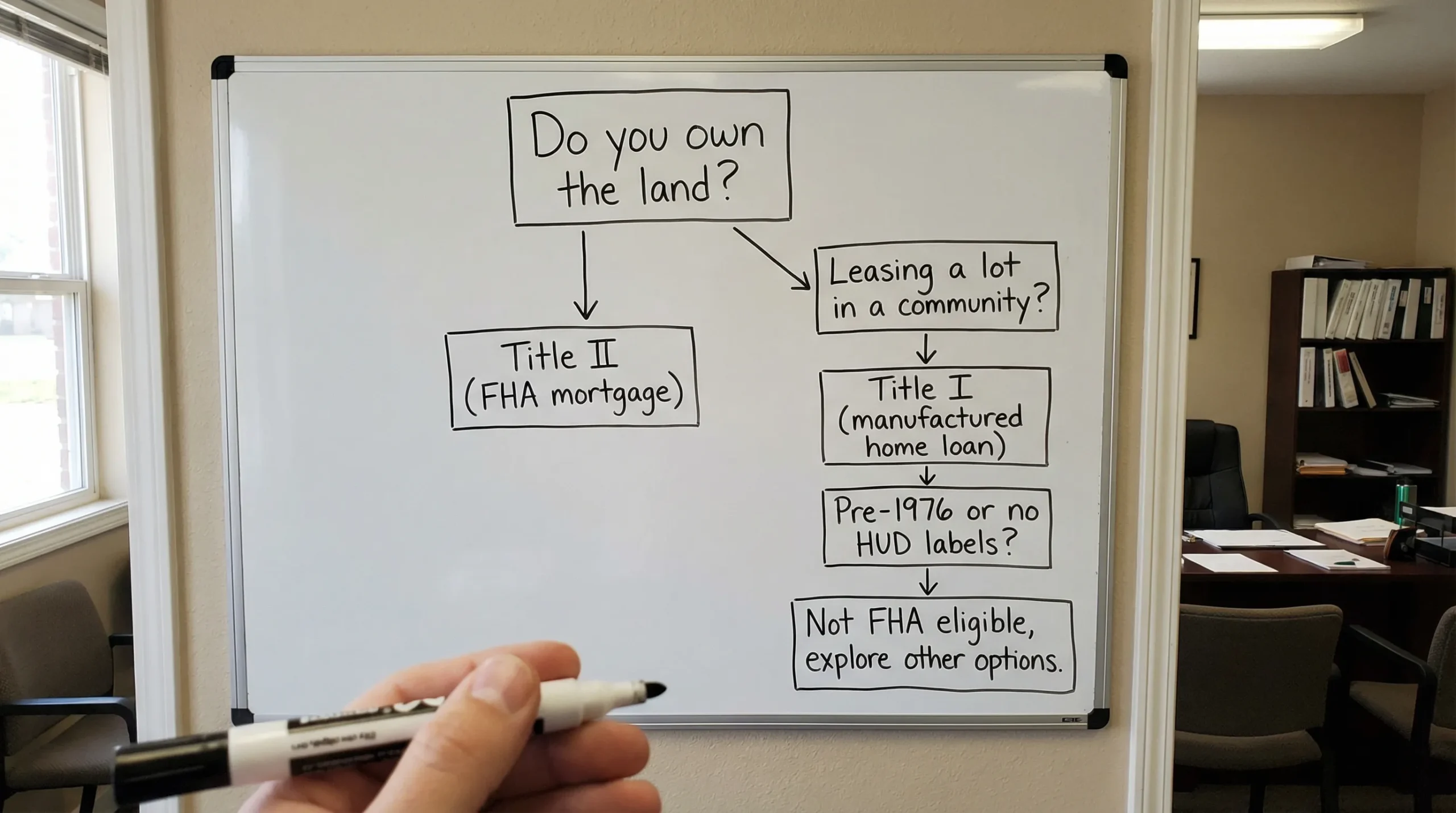

A simple way to choose the right FHA path

If you want a quick decision framework, use this:

- Do you want to own the land and finance everything like a house? You’re likely aiming for FHA Title II, assuming the home can be permanently affixed and properly titled.

- Are you buying the home and placing it in a land-lease community (or not doing a traditional mortgage)? Ask lenders about FHA Title I availability and requirements.

- Is the home pre-1976 or missing HUD documentation? Plan on a different financing path, or consider a different home.

What to budget for (beyond the home price)

Even when FHA financing helps you get in the door, manufactured homes have cost categories buyers sometimes underestimate:

- Site prep (grading, pad, driveway approach, drainage)

- Foundation and installation

- Utility runs (distance can drive cost)

- Engineering/foundation certification if required by the lender

- Appraisal and inspections

- Insurance and taxes (varies based on land ownership and classification)

If energy bills are part of your long-term budget, newer manufactured homes can be a major upgrade, and it’s worth shopping with efficiency in mind. See: Energy-Efficient Manufactured Homes: Save More in Texas Heat.

Step-by-step: how an FHA manufactured home purchase usually plays out

Here’s what the process often looks like for San Antonio area buyers when they want FHA financing and fewer surprises.

- Pick your target setup: community lot (lease) vs private land, and decide whether you want Title I or a Title II mortgage.

- Get prequalified with an FHA-capable lender: confirm which FHA manufactured home options they actually offer.

- Choose an FHA-eligible home model: verify HUD Code compliance and documentation early.

- Confirm site feasibility: utilities, access, zoning/placement rules, and (if applicable) community approval requirements.

- Write the contract with the financing path in mind: timelines for appraisal, installation, and required inspections can be different from site-built homes.

- Appraisal and underwriting: the lender validates borrower docs, and the appraiser checks property acceptability.

- Installation/foundation completion (as required): meet the lender’s and FHA’s requirements for a safe, compliant setup.

- Closing and move-in: coordinate final verification steps (final inspection/clearances, depending on the transaction).

How Homes2Go San Antonio can help

FHA financing for mobile homes is less about memorizing rules and more about matching the right home, the right site, and the right lender program from day one.

Homes2Go San Antonio can help you:

- Compare home models with detailed floor plans and realistic setup considerations

- Understand whether your plan fits better as a land-and-home purchase or a community placement

- Connect with trusted local lenders familiar with manufactured housing in the San Antonio market

If you want to do some additional homework first, start with Homes2Go’s broader overview: Manufactured Homes San Antonio: Options, Prices, Tips. Then, when you’re ready, reach out to the Homes2Go team through the main site to talk through the FHA path that best fits your goals: Homes2Go San Antonio.

Mobile Homes for Rent San Antonio: Where to Look

Mobile Homes for Rent San Antonio: Where to Look How to Find FHA Mobile Home Lenders in Texas

How to Find FHA Mobile Home Lenders in Texas

{kind=link}

{kind=link}

{kind=link}

{kind=link}