Buying a manufactured or mobile home in San Antonio often comes down to one practical question: are you financing the home only, or the home plus the land? That distinction is where chattel loans come in.

Chattel loans for mobile homes can be a smart, straightforward way to get into a move in ready home, especially in land-lease communities or when land financing is not part of the plan. But they are not the best fit for every buyer. This guide breaks down when chattel loans make sense, what you trade off, and how to choose confidently.

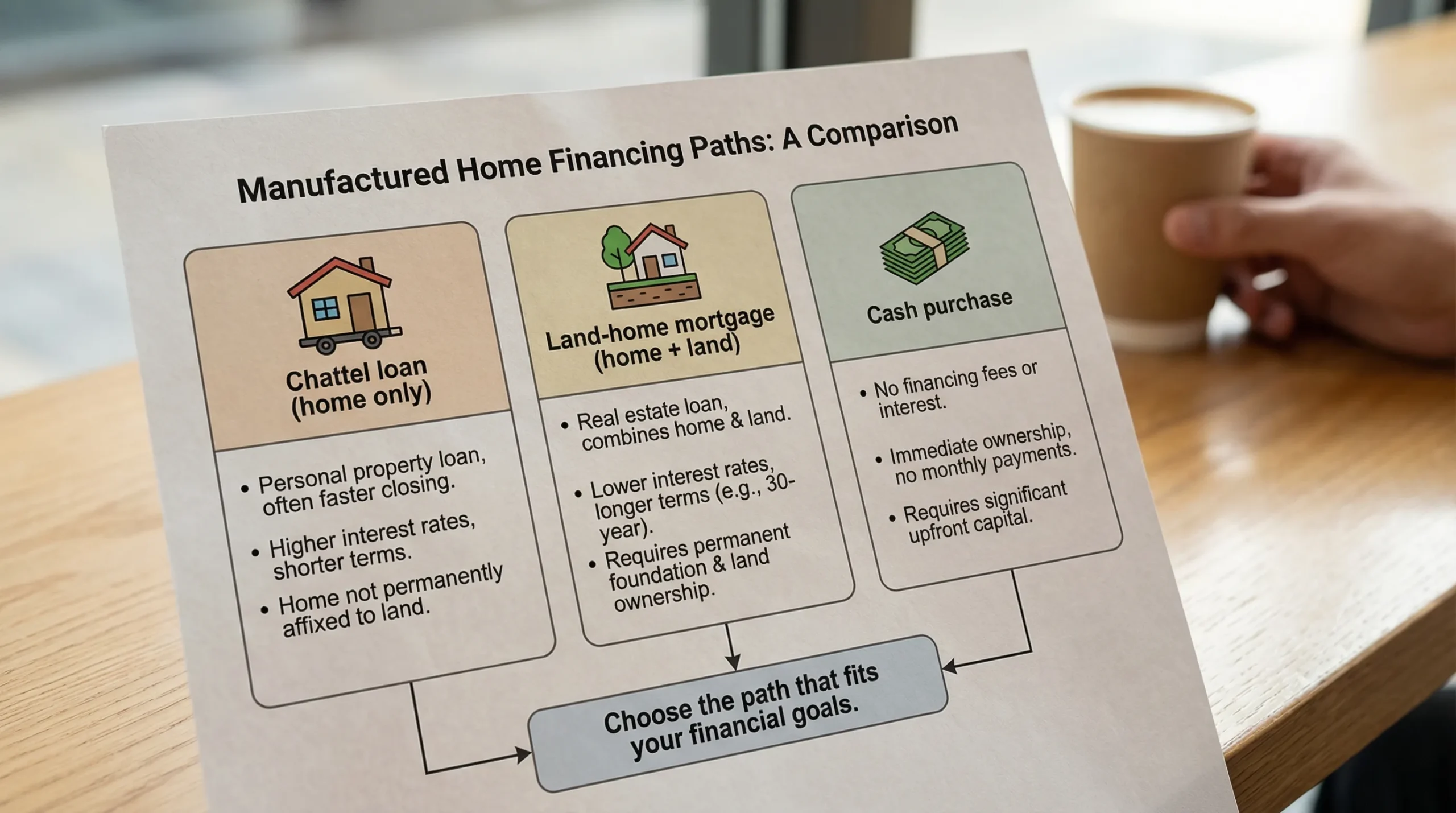

What is a chattel loan for a mobile home?

A chattel loan is financing for personal property. In manufactured housing, that usually means the loan is secured by the home itself, not by the land underneath it.

That structure is common when:

- You are placing the home in a manufactured home community where you lease the lot.

- You are buying a home-only deal and already have land, or you are not purchasing land at the same time.

- The home is titled as personal property (which can be true even if it sits on private land, depending on how it is recorded).

By comparison, a traditional mortgage generally requires that the home be treated as real property and that the loan includes land (or that the home is legally affixed and converted, depending on the program and jurisdiction).

For Texas-specific rules around manufactured housing documentation and titling, the Texas Department of Housing and Community Affairs (TDHCA) Manufactured Housing Division is the key reference point.

When chattel loans make sense (and when they do not)

Chattel financing is not “good” or “bad” on its own. It is a tool that fits certain situations extremely well.

1) You are buying in a land-lease community

If you plan to live in a community where you pay monthly lot rent, a chattel loan is often the most direct financing path because you are not buying the underlying real estate.

This is one of the most common and sensible uses of chattel loans: finance the home, lease the site.

2) You want a simpler home-only transaction

If your move-in plan is straightforward (pick a home model, finalize the home-only purchase, coordinate delivery and setup), chattel loans can be less complex than land-home mortgages.

In many cases, buyers choose chattel financing because it aligns with the reality of the purchase: the home is the primary asset being financed.

3) You need flexibility on land plans

Some buyers intend to purchase land later, or they are still deciding between:

- A community lot today

- Private land later

In those situations, a chattel loan can be a bridge. You get into the home sooner, then revisit long-term land and refinance options when your plan is clearer.

4) The loan amount is relatively small

Manufactured homes can be a more affordable path to homeownership, and sometimes the amount you need to borrow is below what certain mortgage programs comfortably support (especially after you factor in land requirements, appraisal rules, and closing costs).

Chattel loans are frequently used for smaller loan balances, where mortgage-style underwriting might be harder to justify.

5) You are prioritizing speed and certainty

Even when buyers qualify for multiple routes, chattel financing can be appealing if your top priority is:

- A clean, home-focused approval process

- A timeline that matches delivery and installation planning

That said, speed should never be the only deciding factor. The total long-term cost matters.

A quick “fit check” table

| Situation | Why a chattel loan can fit | When to consider another option |

|---|---|---|

| Buying in a land-lease community | You are financing the home only | If you plan to buy land soon and can finance land+home now |

| You already own land but home is not (yet) treated as real property | Chattel can work before conversion | If you can convert to real property first and qualify for a mortgage program |

| First-time buyer focused on payment and move-in timeline | Home-only process can be more direct | If you expect to stay long-term and want maximum equity-building potential |

| You might relocate in the future | Home-only financing can match shorter horizons | If you want long-term fixed mortgage terms tied to land |

The tradeoffs to understand before choosing chattel financing

The biggest mistake buyers make is comparing only the monthly payment. Instead, weigh chattel loans as a package: rate structure, term length, fees, and how the home is titled.

Chattel loans can cost more over time

In general, chattel loans often carry higher interest rates and shorter terms than mortgages, which can raise the total cost of borrowing. Consumer-focused research has also noted that manufactured housing borrowers often face higher financing costs and fewer choices than site-built borrowers.

For background on the broader manufactured housing finance market, see the Consumer Financial Protection Bureau’s overview and reporting on manufactured housing consumer finance.

Equity growth can look different

With a land-home mortgage, you are typically financing a home plus real estate, which historically is more likely to appreciate over long periods (though appreciation is never guaranteed).

With chattel financing:

- You may not be building equity in land.

- Resale value can depend heavily on the home’s condition, community rules, and local demand.

- Some buyers later refinance into a mortgage if they purchase land or convert the home to real property (when eligible).

Fees, insurance, and “real world” costs still matter

Even if the loan is home-only, you still want a clear picture of:

- Installation and site work responsibilities

- Homeowners insurance requirements

- Community fees and lot rent (if applicable)

- Property tax treatment (which may differ based on titling)

These are not reasons to avoid chattel loans. They are reasons to underwrite your decision like a pro, not like a shopper.

Key questions to ask lenders (before you commit)

Chattel loans vary widely by lender, so you will want to compare real terms, not just a quoted payment.

Ask these questions and write the answers down:

- Is this a fixed-rate or adjustable-rate loan? If adjustable, what triggers changes and what are the caps?

- What is the loan term and amortization? (For example, the term length and whether the payment is fully amortizing.)

- What down payment is required, and what counts as down payment?

- Are there origination fees or other finance charges? Ask for an itemized list.

- Is there a prepayment penalty? If yes, how long does it apply and how is it calculated?

- What are the requirements for the home itself? (Age, HUD label/plate, condition, installation standards.)

- What documentation is needed for titling and ownership transfer?

- Can this loan be refinanced later, and what would need to change? (Land purchase, conversion to real property, credit milestones.)

If a lender cannot explain these plainly, it is a sign to slow down.

San Antonio and Texas considerations buyers should not ignore

Texas has its own documentation and compliance landscape for manufactured homes. Without getting lost in legal details, here are the practical points that often affect financing and timelines:

Titling and ownership records matter

Manufactured homes in Texas are commonly tracked through TDHCA Manufactured Housing documentation (including location and ownership records). The way the home is recorded can influence:

- Whether lenders treat it as personal property (chattel) or real property

- How taxes are assessed

- What is required at closing and for future resale

Start your homework at the TDHCA Manufactured Housing Division so you know which documents you may need.

Installation standards can affect lender eligibility

Many lenders require that the home be installed to recognized standards and that key identifiers are present (for example, HUD label information on HUD-code manufactured homes). If you are buying a pre-owned home, confirm what documentation is available early.

Community approval can be part of the process

If you are moving into a land-lease community, there may be separate steps (and timelines) for:

- Community application and approval

- Lot availability and lease signing

- Installation coordination

Financing is only one lane in the move-in timeline.

How to improve your odds of approval (and protect your budget)

If you want better options, focus on the factors lenders typically care about: credit profile, stability, and the condition and documentation of the home.

A few high-impact moves:

- Check your credit reports for errors before applying.

- Reduce revolving balances if possible, even small reductions can help your debt-to-income picture.

- Keep paperwork ready (proof of income, IDs, residence history).

- Choose a home that lenders are comfortable financing (HUD-code, clear documentation, good condition).

Just as important, plan for the non-loan costs that show up after move-in. A simple way to create breathing room is to reduce “surprise spending” categories in your monthly budget. For example, if your household routinely buys convenience snacks, switching to bulk purchases can lower your per-serving cost. Some buyers even stock up through options like bulk beef jerky online to make road trips, work lunches, and moving days cheaper and more predictable.

How Homes2Go San Antonio can help you choose the right financing path

Chattel loans can be a solid fit, but the best choice depends on your full plan: where the home will be placed, whether land is involved, and how you want your long-term costs to look.

Homes2Go San Antonio works with buyers who want a clearer, less stressful process by helping you:

- Compare manufactured home models and floor plans

- Understand which financing direction fits your placement plan (community vs private land)

- Connect with trusted local lenders and explore flexible financing options

- Get guidance through the steps from selection to move-in

If you are still deciding between a home-only purchase and a land-home setup, it can help to talk through both paths before you apply.

Frequently Asked Questions

Are chattel loans for mobile homes only for older homes? Not necessarily. Chattel loans are about how the home is financed (home-only as personal property), not strictly the age of the home. Many buyers use chattel financing for newer manufactured homes placed in land-lease communities.

Do chattel loans always have higher interest rates than mortgages? Often, yes, chattel loans commonly price higher than traditional mortgages because the collateral is the home only and the loan structure differs. The exact rate depends on lender, credit, down payment, and the home.

Can I refinance a chattel loan later into a mortgage? Sometimes. Buyers may refinance if they purchase land, meet program requirements, and the home can be treated as real property under applicable rules and lender guidelines.

Is a chattel loan a bad idea if I plan to stay long-term? Not automatically. It can still make sense, especially in a community you love. The key is comparing total cost, term length, fees, and your long-term plan for land, resale, and refinancing.

Talk with a local team before you decide

If you are weighing chattel loans for mobile homes versus a land-home mortgage, get help mapping the option to your real situation, where the home will go, what you can qualify for, and what costs you should expect.

Explore financing resources and start the conversation with Homes2Go San Antonio here: Homes2Go SA Financing.

Mobile Parks for Rent: Lease Terms You Should Know

Mobile Parks for Rent: Lease Terms You Should Know

{kind=link}

{kind=link}

{kind=link}

{kind=link}